Comerica Incorporated (NYSE: CMA) is a financial services company headquartered in Dallas, Texas, and strategically aligned by three business segments: The Business Bank, The Retail Bank, and Wealth Management. Comerica focuses on relationships, and helping people and businesses be successful. In addition to Texas, Comerica Bank locations can be found in Arizona, California, Florida and Michigan, with select businesses operating in several other states, as well as in Canada and Mexico.

We have taken significant steps to transform our company for the better. As a result of the hard work of our entire team, an action-oriented improvement plan and a sharp focus on results, we emerged from 2016 a stronger and more confident organization, well positioned for the road ahead. This was positively reflected in our stock’s performance and increased profitability as we moved through the year.

As always, we are committed to providing exceptional experiences for our customers and serving as their trusted advisor, while diligently working to reduce costs and drive efficiencies. Although we have consistently posted superior average loans and deposits per employee relative to our peers, we recognized that we needed to do more to improve returns and enhance shareholder value. As a result, in July 2016, we announced a transformational, enterprise-wide initiative to help grow efficiency and revenues, which we call GEAR Up.

Today, GEAR Up is already making a substantial contribution to our bottom line. Through GEAR Up, we identified and began in earnest executing on more than 20 work streams. As promised, we achieved more than $25 million in expense savings in 2016. In total, by the end of 2018, we expect to drive at least $270 million in additional pretax income, relative to when we began the program.

Expanded product offerings, enhanced sales tools and training and better customer analytics are expected to increase customer penetration of our products. We’ve also streamlined leadership across our organization to support speed and simplicity of getting business done, which has resulted in renewed vigor and focus for our colleagues.

We’ve taken a multifaceted approach to cutting costs, including reducing our workforce by approximately nine percent, redesigning our retirement program, optimizing real estate, streamlining operational processes, selectively outsourcing technology functions and reducing technology system applications.

Workforce reductions included the elimination of about 30 percent of our management positions in order to get closer to our customers and accelerate decision making, while ensuring we maintain our high standards for customer service and deep expertise and experience. Our new retirement program continues to provide highly competitive benefits and is expected to contribute approximately $33 million in savings in 2017. We are implementing technological enhancements, such as digitizing our credit processes to enhance data collection and analysis and improve the customer experience, as well as optimizing our infrastructure and substantially reducing the number of IT applications across the bank.

And we have also begun rationalizing our real estate. While we remain committed to our footprint, with the advancement of technology and customers' migration to a broader use of digital channels, we need less space to operate our business. The consolidation of 38 banking centers, or about eight percent of our network, of which four were closed in the second quarter and 15 were closed in the fourth quarter, is expected to result in $10 million to $13 million per annum in savings. This is net of customer attrition, which is expected to be nominal as we have another banking center within two to five miles for the bulk of the locations that are being closed. Also, we have developed a plan to consolidate operations and office space, and are targeting a 500,000-square-foot reduction in real estate, which should result in approximately $7 million in savings in 2018.

Collectively, these actions take us a long way towards our goal of achieving a double-digit return on equity in 2018. We expect to meet or exceed this goal with sustained growth, net of investment, normal credit costs, continued equity buybacks and assuming only a modest increase in rates. In addition, we are targeting an efficiency ratio of at or below 60 percent by year-end 2018 and we believe that the December increase in rates will help us reach this goal even faster. Importantly, while rising rates can be a significant benefit to Comerica, we are committed to these initiatives and are not relying on rate increases or a better economic environment to achieve our objectives.

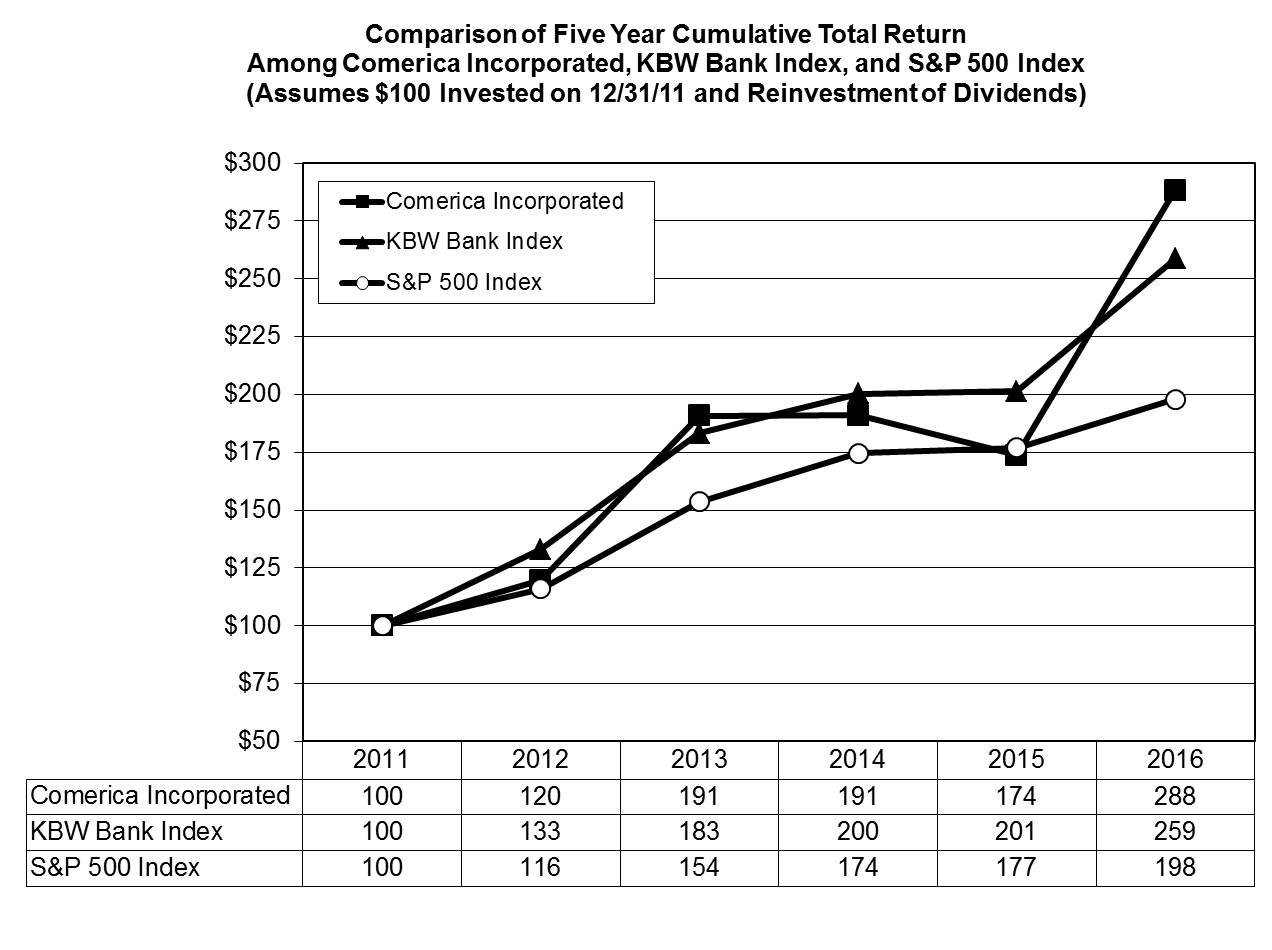

We believe our stock’s performance in part reflects that investors recognize the value of our GEAR Up initiative. In 2016, Comerica's stock increased 63 percent, compared to a year ago, outperforming all of our peers as well as the KBW Index and S&P 500 Index. In fact, in the S&P 500 Index, we were the best performing financial stock and among the top 10 performers overall.

I, along with our executive team, remain very confident that we will continue to meet the financial targets that we have established for GEAR Up. We expect the actions we are taking will ensure that we remain a strong partner and trusted advisor for our clients in the future, while enhancing shareholder value and achieving a higher level of returns for our shareholders.

2016 Financial Highlights

We reported 2016 net income of $477 million or $2.68 per share, which included $0.34 in restructuring charges. Earnings per share increased six percent over 2015, excluding these restructuring charges,* as we began to reap the benefits of our GEAR Up initiatives, as well as rising rates. Also, we increased the size of our equity buyback by 25 percent, which is a reflection of our strong capital position and solid financial performance.

Excluding the $641 million reduction in energy loans, average loans increased over $1 billion or 2 percent. The most notable increases in average loans came from areas where we have deep expertise, such as Commercial Real Estate, National Dealer Services, and Mortgage Banker Finance.

Average deposits have grown 32 percent over the last five years and reflect our focus on building long-term client relationships. In 2016, noninterest-bearing deposits increased $1.7 billion, or 6 percent, while interest-bearing deposits declined $2.2 billion. Altogether, total average deposits declined one percent and reflected the adjustments made in early 2016 for the new Liquidity Coverage Ratio (LCR) requirements, which were mostly offset by significant growth in the third and fourth quarter of 2016.

*Earnings per share decreased 6 percent over 2015, including restructuring charges. For 2016, earnings per share excluding restructuring charges is calculated by taking the net income available to common shareholders ($473 million), plus restructuring charges net of tax ($59 million), divided by diluted average common shares (177 million).

We had $1.8 billion of net interest income in 2016, an increase of 6 percent, primarily the result of higher interest rates, loan growth and a larger securities portfolio, partially offset by modestly higher debt costs.

Credit quality continued to be strong. The provision for credit losses increased primarily due to a larger reserve required for Energy loans in the first quarter of 2016, partially offset by improvements in the remainder of the portfolio. Net charge-offs of 32 basis points were at the low end of our through-the-cycle average, and excluding energy line of business, our net charge-offs were 13 basis points.

With respect to noninterest income, customer-driven fees increased $22 million, or over two percent. We had a large increase in card fees, as well as growth in fiduciary, foreign exchange and brokerage fees as we continue to focus on growing and expanding relationships.

Noninterest expenses declined $23 million after excluding restructuring charges of $93 million, as well as a $33 million release of litigation reserves in 2015. Our GEAR Up initiative drove over $25 million in expense savings.

In June 2016, we announced that the Federal Reserve did not object to our 2016 Capital Plan. In April and July 2016, our board of directors increased the quarterly cash dividend for common stock by 5 percent and 4.5 percent, respectively, to 23 cents per share. We repurchased 6.6 million shares in 2016 under our equity repurchase program. Through the buyback and dividends, we returned $458 million, or 96 percent, of 2016 net income to shareholders. Our regulatory capital levels remain comfortably above the threshold to be considered well-capitalized.

In summary, the skillful execution of our GEAR Up initiative, a modest rise in rates, and a 25 percent increase in our equity repurchase program resulted in a six percent increase in our 2016 earnings per share before restructuring expenses, and improvements in our efficiency ratio and returns on assets and equity. Our book value increased three percent over the past year, to $44.47, and tangible book value per share increased four percent over the past year, to $40.79, as we continue to focus on creating long-term shareholder value.**

**See Supplemental Financial Data section for reconcilements of non-GAAP financial measures.

Relationship Banking Strategy and Balanced Geographic Footprint Keys to Success

Our relationship banking strategy and balanced geographic markets are important drivers of our success. Comerica strives to be the trusted advisor to our clients, providing them with financial products and services they need to prosper. Our geographic footprint is well situated and provides diversity and significant growth opportunities. We remain committed to delivering exceptional customer experiences that exceed expectations and deliver a higher level of banking.

Regarding our footprint, we have a strong presence in the major metropolitan areas of Texas, California and Michigan, providing us with a balanced market presence. We also have locations in Arizona and Florida, with certain businesses operating in several other states, as well as Canada and Mexico. While our unique geographic footprint provides us with economic diversity, we operate as ‘one bank’ and our policies, procedures and systems are integrated across our footprint. A single platform provides significant synergies and is highly efficient and cost effective.

TEXAS: We’ve had a presence in Texas for almost three decades and moved our corporate headquarters to Dallas nearly 10 years ago. We have operations throughout Dallas-Fort Worth, Houston, Austin, and San Antonio. We continue to leverage our standing as the largest U.S. commercial bank headquartered in the state to generate new customer relationships.

The Texas economy has proved to be very resilient in adjusting to the challenging low oil price environment. We believe that the state’s important energy sector is starting to turn the corner, aided by firmer prices and strong demand. We expect Texas to continue to generate new jobs and business opportunities, supported by a healthier energy sector and a stronger U.S. economy in 2017.

CALIFORNIA: We have had a presence in California for more than 25 years. San Jose serves as our market headquarters. Additionally, we have a presence in the Greater San Francisco area, Los Angeles, Orange County, San Diego, Sacramento, and Santa Cruz/Monterey.

We expect California’s economy to be a solid performer in 2017. Expanding U.S. and global economies plus the accelerated diffusion of new technologies into the broader economy will support the state’s important technology sector. Likewise, improving domestic and international economic conditions are positive factors for the state’s entertainment industry.

MICHIGAN: In Michigan, we operate in Detroit, which is our market headquarters, as well as in the Detroit metropolitan area, Ann Arbor, Battle Creek, Grand Rapids, Jackson, Kalamazoo, Lansing, Midland, and Muskegon. We have maintained a continuous presence in Michigan since 1849, and continue to hold the second largest deposit market share in the state, based on the latest FDIC deposit market share survey.

The Michigan economy continues to improve, buoyed by a strengthening manufacturing sector. U.S. auto sales remain strong and the auto industry is in the midst of an exciting surge in new technologies, including the innovation of state-of-the-art “smart car” driving systems. Michigan’s leading academic institutions are playing a key role in developing these new technologies and incubating new business opportunities.

Our Three Strategic Lines of Business

In addition to our diverse footprint, growth is driven by our three strategic lines of business. Our model continues to be weighted toward commercial banking through our Business Bank and complemented by the Retail Bank and Wealth Management.

Within the Business Bank, Middle Market Banking remains our "bread and butter." It is where we have a competitive advantage due to the depth and breadth of our expertise in this area. As part of our GEAR Up initiative, we are taking steps to nationalize our middle market sales process. We are doing this by leveraging our best practices and conducting business in a consistent manner throughout our enterprise. Our focus is on sales enablement, organizational consistency, operational efficiency and talent management. Nationalizing our middle market sales process will be an important initiative for us throughout 2017. And it is expected to result in improved productivities, revenue generation and reduced expenses.

In May, Comerica was honored to be selected by the U.S. Treasury to be their Financial Agent providing merchant card services, also known as Card Acquiring Services. With a five year contract, this business includes approximately 7,000 merchant accounts, representing a multitude of government agencies, and an estimated $12 billion in annual payments volume. This expands our relationship with the U.S. Treasury, which already included DirectExpress®, the program that provides Social Security payments via a pre-paid card, and myRA®, a savings option for those who do not have access to a retirement savings plan at work.

Our Retail Bank continues to focus on ensuring we have the products, services and locations to meet customer needs. In addition to strategically repositioning our banking center network through consolidations and relocations, we completed more than two dozen interior refurbishments in 2016, which included transitions to new design concepts and teller cash recyclers to improve efficiency.

We also successfully deployed transformational technologies at our Greenville banking center in Dallas, building upon the successful deployment of these technologies at banking centers in Michigan and California. Approximately 90 percent of transactions at the Greenville banking center are processed via the ATMs and BankerConnect, our interactive teller-like machine. In addition, we introduced Comerica-branded ATMs at the highly-trafficked Detroit Metropolitan Airport.

Also within the Retail Bank, we made Web Banking and Bill Pay upgrades, including the launch of Web Banking Combined View, which allows our Web Banking customers to combine accounts with different taxpayer identification numbers under one Web Banking ID, fulfilling a significant customer request. Furthermore, we launched a web-based Comerica Insurance Services platform that enables customers to compare shop and buy a variety of insurance products from multiple providers.

Small Business successes in 2016 included the integration of a new centralized underwriting center that supports relationships up to $1.5 million in exposure. This contributed to improved speed-to-market for these types of loans.

Wealth Management enables us to bring private banking, investment management and fiduciary services to our Business Bank and Retail Bank clients. In large part due to our GEAR Up initiative, Wealth Management made notable progress in growing loans and fee income, while controlling expenses, and managing risk appropriately. In 2017, we will launch the Wealth Productivity Transformation initiative, which includes the implementation of a relationship management tool that we believe will enable our colleagues to drive market share and better serve our clients. Wealth Management also expects to leverage technology to increase productivity, increase share of wallet, and reduce time to close.

Well Positioned for Rising Rates

The Federal Reserve increased its benchmark rate 25 basis points in December 2016, marking only the second change it has made to the short-term benchmark rate in eight years. As I previously mentioned, our 2016 financial results benefited meaningfully from the December 2015 rate increase. Comerica's business model continues to be well positioned for a rising rate environment.

Our balance sheet is sensitive to movement in interest rates, since the majority of our revenue is derived from the interest we receive on loans we provide to our clients. Our loan portfolio represents over two-thirds of our total assets as of December 31, 2016, and over 90 percent of our loans are floating rate. Therefore, as rates rise, our portfolio reprices quickly. In addition, more than 50 percent of our deposits are noninterest-bearing, and, as such, are less impacted by movement in rates. They also provide us a source of low-cost funding as loan growth continues.

Energy Portfolio Weathering the Cycle

At year-end 2016, our energy loans had declined $820 million, or 27 percent, from one year ago, bringing our Energy line of business to less than five percent of our total loans. Energy Services, which has been most significantly impacted this cycle, represented less than one percent of our total loan portfolio. The performance of our Energy portfolio has improved. While oil prices have been relatively stable, we continue to be cautious and believe we are properly reserved with our loan loss reserve allocation at over seven percent of Energy loans as of December 31, 2016. We remain committed to the energy sector and believe that in cycles such as the current one, we can further cement our relationship with our clients.

Recent Additions Enhance Strong Board

Our board appointed two new independent directors in 2016: Michael Van de Ven, who is the chief operating officer of Southwest Airlines, and Mike Collins, who had a distinguished 37-year career at the Federal Reserve Bank of Philadelphia. We have a strong and diverse board with a good mix of industry, financial and leadership backgrounds. Given the regulated nature of our industry as well as its cyclicality, we believe it is important to have long-tenured directors with a deep understanding of our business and environment. However, we also recognize the importance of bringing fresh perspectives.

Investments in Cybersecurity Continue

The cybersecurity threat environment is intensifying and Comerica's defenses are ready. Over the past several years, Comerica has met this escalating environment with significant investments in its cybersecurity defensive posture, building a robust program with advanced identification, protection, detection, response and recovery capabilities. We have established a cybersecurity capability that leverages industry standard frameworks and targeted regulatory guidance to provide wide coverage, which we evaluate regularly through independent assessments. Our security operations center and intelligence capabilities are monitoring our systems 24/7, constantly adjusting our defenses to the changing threat environment.

Opportunities for Regulatory Relief

The national election is bringing change to Washington, D.C. and with it, optimism for regulatory relief for banks, particularly those of our size. It now appears to be a legislative priority to reduce complex and costly regulations that burden banks and impact the flow of credit to businesses. We believe there is potential for revision or elimination of certain aspects of the Dodd-Frank Wall Street Reform and Consumer Protection Act that could benefit Comerica and the industry as a whole. This includes changes to the definition of a systemically important financial institution (SIFI) from the current $50 billion and above in assets to either a higher asset threshold or a metrics-based formula to determine a firm's true complexity and risk profile. We believe a positive change to the SIFI designation would be a major step toward the kind of regulatory relief that would potentially spur increased lending to businesses, reduce compliance expenses, and allow us to manage capital and liquidity to meet our needs in a more prudent manner.

Our Strong Commitment to Community, Diversity, Financial Literacy and Sustainability

Comerica continued its commitment to the communities in which we operate in 2016. Comerica contributed more than $8 million to not-for-profit organizations in the markets we serve, and, in addition, our employees raised nearly $1.7 million for the United Way and Black United Fund. Our team also donated their personal time and talents - about $1.3 million worth in volunteer hours - to make a positive difference in our local communities.

Some of the recognition we received for our efforts included the prestigious Corporate Social Responsibility Award from the Financial Services Roundtable. In addition, Comerica was named as one of the 50 most community-minded companies in the nation as part of the Civic 50, an initiative of Points of Light, the world's largest organization dedicated to volunteer service.

Our community “Shred Day” events continue to serve as the largest, most visible and most successful brand awareness, public education, colleague engagement, and community service campaigns that we host. Working with event partner Iron Mountain at shred-day events in Dallas, Houston, Phoenix and Detroit, we securely destroyed and recycled more than 800,000 pounds of paper in 2016, while gathering donations for local food banks. These signature events continue to provide a triple bottom line: helping reduce fraud and identity theft, freeing up hundreds of tons of space in local landfills, and raising awareness of hunger in our communities.

We marked the fifth year of the Comerica Hatch Detroit Contest by more than doubling our commitment. In addition to providing the grand prize for the winning idea for a new retail business, we invested funds to help launch even more small businesses in the city. Fifteen new businesses are now open, thanks to the contest's success. We sponsored a similar contest in Dallas with the Dallas Entrepreneur Center and Tech Wildcatters. These contests offer us an opportunity to advance the aspirations of entrepreneurs in our markets.

Diversity is an important core value at Comerica. We support 39 diversity-focused teams within the bank that promote employee engagement, business outreach, and diversity awareness and learning among colleagues. Comerica's focus on diversity has been favorably recognized, as we earned a third consecutive perfect 100 rating on the Human Rights Campaign Foundation's 2017 Corporate Equality Index, a national benchmarking survey and report on corporate policies and practices related to LGBT workplace equality.

Black Enterprise magazine placed Comerica on its 2016 “40 Best Companies for Diversity” list. Comerica also ranked No. 2 on the DiversityInc 2016 Top 10 Regional Companies for Diversity. In addition, we were named to LATINO magazine’s 2016 “LATINO 100” list, the fourth annual listing of the top 100 companies providing the most opportunities for Latinos in such areas as education, hiring, workforce diversity, minority business development, governance and philanthropy.

We also ranked among 2016's "Best Places for Women and Diverse Managers to Work" by Diversity MBA, which is a national leadership organization targeting leadership and talent management among professionals, managers and executives. In addition, Comerica was named among the "Top 25 Companies for Diversity in Texas" by the National Diversity Council. The award is based on women and minority representation in executive leadership and on boards of directors.

We continued to expand our financial education efforts throughout our footprint in 2016, with some impressive results. The Comerica Money $ense program, which has been incorporated into the classrooms of 41 elementary schools throughout Maricopa, Palm Beach and Broward counties in Florida, is a web-based financial education program designed by leading technology company, EverFi. During the 2015-2016 school year, more than 2,100 students were served by the Comerica-funded program, with more than 6,000 learning modules completed to help predominantly low- and moderate-income students learn how to make wise financial decisions.

Comerica recognizes the business value created through sustainability and that’s why it is embedded in our core values. We continued our progress on reducing our environmental footprint in line with Comerica’s 2020 Environmental Sustainability Goals and remain ahead of pace on our efforts to reduce greenhouse gas emissions, water consumption, and paper use by 2020. In addition, we exceeded our goal of reducing waste sent to the landfill four years ahead of schedule by achieving a 24.1 percent reduction compared to our goal of 20 percent. Also, Comerica continues to support a green economy with nearly $900 million of environmentally beneficial loans and commitments to companies in 13 different categories.

In 2016, we were once again recognized for our climate change management strategy and emissions reduction efforts through CDP (formerly known as the Carbon Disclosure Project), receiving an “A-“ rating, among the highest scores in the U.S. financial services industry. Our work on supply chain sustainability earned Comerica its third consecutive Green Supply Chain Award from Supply & Demand Chain Executive magazine, and we were pleased to be listed on the FTSE4Good index series for the 8th consecutive year.

Positioned for Future Growth

In closing, 2016 was a pivotal year with the development and implementation of our enterprise-wide GEAR Up initiative. We have made significant progress in executing the expense savings and are fully committed to delivering on the efficiency and revenue opportunities to further enhance our profitability and shareholder value. We also benefited meaningfully from increased interest rates and our overall credit metrics remained strong as we continued to navigate the energy cycle. In addition, there has been much discussion in Washington, D.C. about plans to reduce taxes, provide regulatory relief and fiscal stimulus to drive economic growth. While there is no certainty as to what changes may prevail, we believe our customers and Comerica should benefit if changes are made. We believe we are well positioned for the future as our geographic footprint is well situated and our relationship banking strategy can drive superior growth of loans, deposits and fee income over time.

Thank you for your continued support.

(1) Audit Committee

(2) Governance, Compensation and Nominating Committee

(3) Qualified Legal Compliance Committee

(4) Enterprise Risk Committee

* Committee Chairperson

|

Delaware |

38-1998421 | |

|

(State

or Other Jurisdiction of Incorporation) |

(IRS

Employer Identification

Number) | |

|

Large

accelerated

filer ý |

Accelerated

filer o |

Non-accelerated

filer o

(Do not

check if a smaller

reporting

company) |

Smaller

reporting

company o | |||

|

F-1 | |

|

S-1 | |

|

E-1 | |

|

• |

People: Including the

competence, integrity and succession planning of

customers. |

|

• |

Purpose: The legal, logical

and productive purposes of the credit

facility. |

|

• |

Payment: Including the

source, timing and probability of

payment. |

|

• |

Protection: Including

obtaining alternative sources of repayment, securing the loan, as

appropriate, with collateral and/or third-party guarantees and ensuring

appropriate legal documentation is

obtained. |

|

• |

Perspective: The

risk/reward relationship and pricing elements (cost of funds; servicing

costs; time value of money; credit risk). |

|

• |

The borrower's business

model. |

|

• |

Periodic review of

financial statements including financial statements audited by an

independent certified public accountant when

appropriate. |

|

• |

The pro-forma financial

condition including financial

projections. |

|

• |

The borrower's sources and

uses of funds. |

|

• |

The borrower's debt service

capacity. |

|

• |

The guarantor's financial

strength. |

|

• |

A comprehensive review of

the quality and value of collateral, including independent third-party

appraisals of machinery and equipment and commercial real estate, as

appropriate, to determine the advance

rates. |

|

• |

Physical inspection of

collateral and audits of receivables, as

appropriate. |

|

• |

General

political, economic or industry conditions, either domestically or

internationally, may be less favorable than

expected. |

|

• |

Governmental

monetary and fiscal policies may adversely affect the financial services

industry, and therefore impact Comerica's financial condition and results

of operations. |

|

• |

Proposed

revenue enhancements and efficiency improvements may not be

achieved. |

|

• |

Comerica

must maintain adequate sources of funding and liquidity to meet regulatory

expectations, support its operations and fund outstanding

liabilities. |

|

• |

Compliance

with more stringent capital and liquidity requirements may adversely

affect Comerica. |

|

• |

Declines

in the businesses or industries of Comerica's customers - in particular,

the energy industry - could cause increased credit losses or decreased

loan balances, which could adversely affect

Comerica. |

|

• |

Unfavorable

developments concerning credit quality could adversely affect Comerica's

financial results. |

|

• |

Operational

difficulties, failure of technology infrastructure or information security

incidents could adversely affect Comerica's business and

operations. |

|

• |

Comerica

relies on other companies to provide certain key components of its

business infrastructure, and certain failures could materially adversely

affect operations. |

|

• |

Changes

in the financial markets, including fluctuations in interest rates and

their impact on deposit pricing, could adversely affect Comerica's net

interest income and balance sheet. |

|

• |

Reduction

in our credit ratings could adversely affect Comerica and/or the holders

of its securities. |

|

• |

The

soundness of other financial institutions could adversely affect

Comerica. |

|

• |

The

introduction, implementation, withdrawal, success and timing of business

initiatives and strategies may be less successful or may be different than

anticipated, which could adversely affect Comerica's

business. |

|

• |

Damage

to Comerica’s reputation could damage its

businesses. |

|

• |

Comerica

may not be able to utilize technology to efficiently and effectively

develop, market, and deliver new products and services to its customers.

|

|

• |

Competitive

product and pricing pressures among financial institutions within

Comerica's markets may change. |

|

• |

Changes

in customer behavior may adversely impact Comerica's business, financial

condition and results of operations. |

|

• |

Any

future strategic acquisitions or divestitures may present certain risks to

Comerica's business and operations. |

|

• |

Management's

ability to maintain and expand customer relationships may differ from

expectations. |

|

• |

Management's

ability to retain key officers and employees may

change. |

|

• |

Legal

and regulatory proceedings and related matters with respect to the

financial services industry, including those directly involving Comerica

and its subsidiaries, could adversely affect Comerica or the financial

services industry in general. |

|

• |

Methods

of reducing risk exposures might not be

effective. |

|

• |

Terrorist

activities or other hostilities may adversely affect the general economy,

financial and capital markets, specific industries, and

Comerica. |

|

• |

Catastrophic

events, including, but not limited to, hurricanes, tornadoes, earthquakes,

fires, droughts and floods, may adversely affect the general economy,

financial and capital markets, specific industries, and

Comerica. |

|

• |

The tax

treatment of corporations could be subject to potential legislative,

administrative or judicial changes or

interpretations. |

|

• |

Changes

in accounting standards could materially impact Comerica's financial

statements. |

|

• |

Comerica's

accounting policies and processes are critical to the reporting of

financial condition and results of operations. They require management to

make estimates about matters that are uncertain.

|

|

Quarter |

High |

Low |

Dividends Per

Share |

Dividend Yield* | |||||||||||

|

2016 |

|||||||||||||||

|

Fourth |

$ |

70.44 |

|

$ |

46.75 |

|

$ |

0.23 |

|

1.6 |

% | ||||

|

Third |

47.81 |

|

38.39 |

|

0.23 |

|

2.1 |

| |||||||

|

Second |

47.55 |

|

36.27 |

|

0.22 |

|

2.1 |

| |||||||

|

First |

41.74 |

|

30.48 |

|

0.21 |

|

2.3 |

| |||||||

|

2015 |

|||||||||||||||

|

Fourth |

$ |

47.44 |

|

$ |

39.52 |

|

$ |

0.21 |

|

1.9 |

% | ||||

|

Third |

52.93 |

|

40.01 |

|

0.21 |

|

1.8 |

| |||||||

|

Second |

53.45 |

|

44.38 |

|

0.21 |

|

1.7 |

| |||||||

|

First |

47.94 |

|

40.09 |

|

0.20 |

|

1.8 |

| |||||||

|

*

Dividend yield is calculated by annualizing the quarterly dividend per

share and dividing by an average of the high and low price in the

quarter. | |||||||||||||||

|

(shares

in thousands) |

Total Number of Shares

and

Warrants Purchased

as Part

of Publicly

Announced

Repurchase

Plans

or Programs (a) |

Remaining

Repurchase

Authorization

(b) |

Total Number

of

Shares

Purchased

(c) |

Average

Price

Paid Per

Share | ||||||||

|

Total

first quarter 2016 |

1,183 |

|

15,721 |

|

1,393 |

|

$ |

35.26 |

| |||

|

Total

second quarter 2016 |

1,483 |

|

14,238 |

|

1,488 |

|

43.78 |

| ||||

|

Total

third quarter 2016 |

2,123 |

|

22,114 |

|

(d) |

2,134 |

|

45.66 |

| |||

|

October

2016 |

839 |

|

19,575 |

|

842 |

|

49.88 |

| ||||

|

November

2016 |

644 |

|

17,834 |

|

645 |

|

57.10 |

| ||||

|

December

2016 |

302 |

|

15,694 |

|

307 |

|

67.27 |

| ||||

|

Total

fourth quarter 2016 |

1,785 |

|

15,694 |

|

1,794 |

|

55.45 |

| ||||

|

Total

2016 |

6,574 |

|

15,694 |

|

6,809 |

|

$ |

45.70 |

| |||

|

(a) |

Comerica

made no repurchases of warrants under the repurchase program during the

year ended December 31,

2016.

Upon exercise of a warrant, the number of shares with a value equal to the

aggregate exercise price is withheld from an exercising warrant holder as

payment (known as a "net exercise provision"). During the year ended

December 31,

2016,

Comerica withheld the equivalent of approximately 2,319,000 shares

to cover an aggregate of $68.2

million

in exercise price and issued approximately 2,317,000 shares

to the exercising warrant holders. Shares withheld in connection with the

net exercise provision are not included in the total number of shares or

warrants purchased in the above table. |

|

(b) |

Maximum

number of shares and warrants that may yet be purchased under the publicly

announced plans or programs. |

|

(c) |

Includes

approximately 235,000 shares

(including 9,000 shares

in the quarter ended December 31,

2016)

purchased pursuant to deferred compensation plans and shares purchased

from employees to pay for taxes related to restricted stock vesting under

the terms of an employee share-based compensation plan and 26 shares

purchased by affiliated purchasers through employee benefits plan

transactions during the year ended December 31,

2016.

These transactions are not considered part of Comerica's repurchase

program. |

|

(d) |

Includes

July 26, 2016 equity repurchase authorization for up to an additional 10.0

million shares. |

|

1. |

Financial

Statements: The financial statements that are filed as part of this report

are included in the Financial Section on pages F-44 through

F-111. | |

|

2. |

All

of the schedules for which provision is made in the applicable accounting

regulations of the SEC are either not required under the related

instruction, the required information is contained elsewhere in the

Form 10-K, or the schedules are inapplicable and therefore have been

omitted. | |

|

3. |

Exhibits:

The exhibits listed on the Exhibit Index on pages E-1 through E-5 of this

Form 10-K are filed with this report or are incorporated herein by

reference. | |

The

performance shown on the graph is not necessarily indicative of future

performance.

The

performance shown on the graph is not necessarily indicative of future

performance.|

(dollar

amounts in millions, except per share data) |

|||||||||||||||||||

|

Years

Ended December 31 |

2016 |

2015 |

2014 |

2013 |

2012 | ||||||||||||||

|

EARNINGS

SUMMARY |

|||||||||||||||||||

|

Net

interest income |

$ |

1,797 |

|

$ |

1,689 |

|

$ |

1,655 |

|

$ |

1,672 |

|

$ |

1,728 |

| ||||

|

Provision

for credit losses |

248 |

|

147 |

|

27 |

|

46 |

|

79 |

| |||||||||

|

Noninterest

income (a) |

1,051 |

|

1,035 |

|

857 |

|

874 |

|

863 |

| |||||||||

|

Noninterest

expenses (a) |

1,930 |

|

(b) |

1,827 |

|

1,615 |

|

1,714 |

|

1,750 |

| ||||||||

|

Provision

for income taxes |

193 |

|

229 |

|

277 |

|

245 |

|

241 |

| |||||||||

|

Net

income |

477 |

|

521 |

|

593 |

|

541 |

|

521 |

| |||||||||

|

Net

income attributable to common shares |

473 |

|

515 |

|

586 |

|

533 |

|

515 |

| |||||||||

|

PER

SHARE OF COMMON STOCK |

|||||||||||||||||||

|

Diluted

earnings per common share |

$ |

2.68 |

|

$ |

2.84 |

|

$ |

3.16 |

|

$ |

2.85 |

|

$ |

2.67 |

| ||||

|

Cash

dividends declared |

0.89 |

|

0.83 |

|

0.79 |

|

0.68 |

|

0.55 |

| |||||||||

|

Common

shareholders’ equity |

44.47 |

|

43.03 |

|

41.35 |

|

39.22 |

|

36.86 |

| |||||||||

|

Tangible

common equity (c) |

40.79 |

|

39.33 |

|

37.72 |

|

35.64 |

|

33.36 |

| |||||||||

|

Market

value |

68.11 |

|

41.83 |

|

46.84 |

|

47.54 |

|

30.34 |

| |||||||||

|

Average

diluted shares (in millions) |

177 |

|

181 |

|

185 |

|

187 |

|

192 |

| |||||||||

|

YEAR-END

BALANCES |

|||||||||||||||||||

|

Total

assets |

$ |

72,978 |

|

$ |

71,877 |

|

$ |

69,186 |

|

$ |

65,224 |

|

$ |

65,066 |

| ||||

|

Total

earning assets |

67,518 |

|

66,687 |

|

63,788 |

|

60,200 |

|

59,618 |

| |||||||||

|

Total

loans |

49,088 |

|

49,084 |

|

48,593 |

|

45,470 |

|

46,057 |

| |||||||||

|

Total

deposits |

58,985 |

|

59,853 |

|

57,486 |

|

53,292 |

|

52,191 |

| |||||||||

|

Total

medium- and long-term debt |

5,160 |

|

3,058 |

|

2,675 |

|

3,543 |

|

4,720 |

| |||||||||

|

Total

common shareholders’ equity |

7,796 |

|

7,560 |

|

7,402 |

|

7,150 |

|

6,939 |

| |||||||||

|

AVERAGE

BALANCES |

|||||||||||||||||||

|

Total

assets |

$ |

71,743 |

|

$ |

70,247 |

|

$ |

66,336 |

|

$ |

63,933 |

|

$ |

62,569 |

| ||||

|

Total

earning assets |

66,545 |

|

65,129 |

|

61,560 |

|

59,091 |

|

57,483 |

| |||||||||

|

Total

loans |

48,996 |

|

48,628 |

|

46,588 |

|

44,412 |

|

43,306 |

| |||||||||

|

Total

deposits |

57,741 |

|

58,326 |

|

54,784 |

|

51,711 |

|

49,533 |

| |||||||||

|

Total

medium- and long-term debt |

4,917 |

|

2,905 |

|

2,963 |

|

3,972 |

|

4,818 |

| |||||||||

|

Total

common shareholders’ equity |

7,674 |

|

7,534 |

|

7,373 |

|

6,965 |

|

7,009 |

| |||||||||

|

CREDIT

QUALITY |

|||||||||||||||||||

|

Total

allowance for credit losses |

$ |

771 |

|

$ |

679 |

|

$ |

635 |

|

$ |

634 |

|

$ |

661 |

| ||||

|

Total

nonperforming loans |

590 |

|

379 |

|

290 |

|

374 |

|

541 |

| |||||||||

|

Foreclosed

property |

17 |

|

12 |

|

10 |

|

9 |

|

54 |

| |||||||||

|

Total

nonperforming assets |

607 |

|

391 |

|

300 |

|

383 |

|

595 |

| |||||||||

|

Net

credit-related charge-offs |

157 |

|

101 |

|

25 |

|

73 |

|

170 |

| |||||||||

|

Net credit-related

charge-offs as a percentage of average total loans |

0.32 |

% |

0.21 |

% |

0.05 |

% |

0.16 |

% |

0.39 |

% | |||||||||

|

Allowance for loan losses as

a percentage of total period-end loans |

1.49 |

|

1.29 |

|

1.22 |

|

1.32 |

|

1.37 |

| |||||||||

|

Allowance for loan losses as

a percentage of total nonperforming loans |

124 |

|

167 |

|

205 |

|

160 |

|

116 |

| |||||||||

|

RATIOS |

|||||||||||||||||||

|

Net

interest margin (fully taxable equivalent) |

2.71 |

% |

2.60 |

% |

2.70 |

% |

2.84 |

% |

3.03 |

% | |||||||||

|

Return

on average assets |

0.67 |

|

0.74 |

|

0.89 |

|

0.85 |

|

0.83 |

| |||||||||

|

Return

on average common shareholders’ equity |

6.22 |

|

6.91 |

|

8.05 |

|

7.76 |

|

7.43 |

| |||||||||

|

Dividend

payout ratio |

32.48 |

|

28.33 |

|

24.09 |

|

23.29 |

|

20.52 |

| |||||||||

|

Average common shareholders’

equity as a percentage of average assets |

10.70 |

|

10.73 |

|

11.11 |

|

10.90 |

|

11.21 |

| |||||||||

|

Common equity tier 1 capital

as a percentage of risk-weighted assets (d) |

11.09 |

|

10.54 |

|

n/a |

|

n/a |

|

n/a |

| |||||||||

|

Tier

1 capital as a percentage of risk-weighted assets (d) |

11.09 |

|

10.54 |

|

10.50 |

|

10.64 |

|

10.14 |

| |||||||||

|

Common

equity ratio |

10.68 |

|

10.52 |

|

10.70 |

|

10.97 |

|

10.67 |

| |||||||||

|

Tangible

common equity as a percentage of tangible assets (c) |

9.89 |

|

9.70 |

|

9.85 |

|

10.07 |

|

9.76 |

| |||||||||

|

(a) |

Effective

January 1, 2015, contractual changes to a card program resulted in a

change to the accounting presentation of the related revenues and

expenses. The effect of this change was an increase of $177 million in

2015 to both noninterest income and noninterest expenses. Amounts prior to

2015 reflect revenues from this card program net of related noninterest

expenses. |

|

(b) |

Noninterest

expenses in 2016 included restructuring charges of $93

million. |

|

(c) |

See

Supplemental Financial Data section for reconcilements of non-GAAP

financial measures. |

|

(d) |

Ratios

calculated based on the risk-based capital requirements in effect at the

time. The U.S. implementation of the Basel III regulatory capital

framework became effective on January 1, 2015, with transitional

provisions. |

|

• |

2016 progress included a

reduction in workforce and a significant reduction in retirement plan

expense due to a new retirement program, which together resulted in 2016

expense savings of more than $25 million, as well as the consolidation of

19 banking centers. For additional information regarding retirement plan

changes, refer to the "Critical Accounting Policies" section of this

financial review and Note 17 to the consolidated

financial statements. |

|

• |

Expense reductions are

expected to save an additional $125 million in full-year 2017, relative to

the 2016 GEAR Up savings of more than $25 million, and increase to

approximately $200 million in full-year 2018. This is to be achieved

through continued savings from the reduction in workforce and the new

retirement program, streamlining operational processes, real estate

optimization, including consolidating an additional 19 banking centers in

2017 as well as reducing office and operations space, selective

outsourcing of technology functions and reduction of technology system

applications. |

|

• |

Revenue enhancements are

expected to ramp-up to approximately $30 million in full-year 2017,

gradually increasing to approximately $70 million in full-year 2018,

through expanded product offerings, enhanced sales tools and training and

improved customer analytics to drive

opportunities. |

|

• |

Pre-tax restructuring

charges of $140 million to $160 million in total are expected to be

incurred through 2018. This includes restructuring charges totaling

$93

million, which

were incurred through December 31,

2016, and an

additional $25 million to $50 million expected in 2017. For additional

information regarding restructuring charges, refer to Note 22

to the consolidated financial statements. |

|

• |

Net income was $477 million in 2016, a decrease of

$44

million, or

8

percent,

compared to $521 million in 2015. Net income per diluted

common share was $2.68 in 2016, compared to $2.84

in 2015.

Excluding the after-tax impact of restructuring charges associated with

GEAR Up of $59 million, or $0.34 per share, net income increased $15

million, or 3 percent. |

|

• |

Average loans were

$49.0

billion in

2016,

an increase of $368 million, or 1

percent,

compared to 2015.

Excluding a $641 million decrease in Energy, average loans increased $1.0

billion, primarily reflecting increases in Commercial Real Estate,

National Dealer Services and Mortgage Banker Finance, partially offset by

decreases in general Middle Market and Corporate

Banking. |

|

• |

Average deposits decreased

$585

million, or

1

percent, to

$57.7

billion in

2016,

compared to 2015.

The decrease in average deposits reflected a decrease of $2.2 billion, or 7

percent, in

interest-bearing deposits, partially offset by an increase of $1.7 billion, or 6

percent, in

average noninterest-bearing deposits. The decrease in interest-bearing

deposits reflected decreases of $1.3

billion, or

6

percent, in

money market and interest-bearing checking deposits and $1.0 billion, or 24

percent, in

customer certificates of deposit. The decrease in average deposits

primarily reflected purposeful pricing discipline and strategic actions in

light of new Liquidity Coverage Ratio (LCR) rules, with the largest

decreases in |

|

• |

Net interest income was

$1.8

billion in

2016,

an increase

of $108

million, or

6

percent,

compared to 2015.

The increase

in net interest income resulted primarily from higher interest rates, loan

growth and a larger securities portfolio, partially offset by higher debt

costs. |

|

• |

The provision for credit

losses was $248 million in 2016, an increase of

$101

million

compared to 2015,

primarily reflecting increased reserves for Energy and energy-related

loans recorded in the first quarter 2016, partially offset by improved

credit quality in the remainder of the portfolio. Net credit-related

charge-offs were $157

million, or

0.32

percent of

average loans, for 2016, an increase of

$46

million

compared to 2015.

The increase was primarily due to an increase in charge-offs in the Energy

portfolio. |

|

• |

Noninterest income

increased $16

million, or

2

percent, in

2016,

compared to 2015.

Customer-driven fees increased $22 million and non-fee categories declined

$6 million. An increase in card fees as well as growth in fiduciary,

customer derivative and foreign exchange income was partially offset by

lower commercial lending fees and investment banking

income. |

|

• |

Noninterest expenses

increased $103

million, or

6

percent, in

2016,

compared to 2015.

Excluding $93

million of

restructuring charges related to the GEAR Up initiative and $33 million from the net release of

litigation reserves in 2015, noninterest expenses

decreased $23

million. This

primarily reflected a decrease of $48

million in

salaries and benefits expense, including GEAR Up savings estimated to be

in excess of $25 million as well as an additional decrease in pension

expense, partially offset by the impact of merit increases and one

additional day in 2016. Additionally, increases

in technology expense, outside processing fees and FDIC insurance premiums

were partially offset by decreases in state business taxes and gains from

the early termination of leveraged lease

transactions. |

|

• |

The provision for income

taxes decreased $36

million in

2016,

compared to 2015.

The effective tax rate was 28.8 percent in 2016, compared to 30.5 percent

in 2015,

primarily reflecting a $10 million increase in tax benefits from the early

termination of certain leveraged lease

transactions. |

|

• |

The quarterly dividend was

increased to 22 cents

per share in April 2016 and to 23

cents per

share in July 2016. |

|

• |

The Corporation repurchased

approximately 6.6 million shares of common stock

during 2016

under the equity repurchase program. Together with dividends of

$0.89

per share, $458 million, or 96

percent of

2016

net income, was returned to shareholders. |

|

• |

Average loans higher, in

line with Gross Domestic Product growth, reflecting increases in most

lines of business and reduced headwinds from a declining Energy

portfolio. |

|

• |

Net interest income higher,

reflecting the benefit from the December 2016 short-term rate increase and

loan growth, partially offset by higher funding costs and minor loan yield

comparison. |

|

◦ |

Full-year benefit from the

December rise in short-term rates expected to be more than $70 million,

assuming a 25 percent deposit beta. |

|

• |

Provision for credit losses

lower, with continued solid performance of the overall

portfolio. |

|

◦ |

Provision and net

charge-offs in line with historical normal levels of 30-40 basis

points. |

|

• |

Noninterest income higher,

with the execution of GEAR Up opportunities, modest growth in treasury

management and card fees, as well as wealth management products such as

fiduciary and brokerage services. |

|

◦ |

Increase of 4 percent to 6

percent. |

|

• |

Noninterest expenses lower,

reflecting lower restructuring charges and an additional $125 million in

GEAR Up savings, relative to 2016 GEAR Up savings of more than $25

million. Outside processing is expected to increase in line with growing

revenue. Headwinds include increased technology costs and higher FDIC

insurance expense, as well as typical inflationary pressure. The gains of

$13 million in 2016 from early terminations of certain leveraged lease

transactions are not expected to repeat. |

|

◦ |

Restructuring charges of

$25 million to $50 million, compared to $93 million in

2016. |

|

◦ |

Remaining noninterest

expenses 1 percent to 2 percent lower. |

|

◦ |

Decrease of 4 percent to 5

percent including restructuring charges. |

|

• |

Income tax expense to

approximate 33 percent of pre-tax income excluding the impact of discrete

items such as the tax benefit related to stock compensation of

approximately $14 million recorded during January

2017. |

|

(dollar

amounts in millions) |

||||||||||||||||||||||||||

|

Years

Ended December 31 |

2016 |

2015 |

2014 | |||||||||||||||||||||||

|

Average

Balance |

Interest |

Average

Rate

(a) |

Average

Balance |

Interest |

Average

Rate

(a) |

Average

Balance |

Interest |

Average

Rate

(a) | ||||||||||||||||||

|

Commercial

loans |

$ |

31,062 |

|

$ |

1,008 |

|

3.26 |

% |

$ |

31,501 |

|

$ |

962 |

|

3.07 |

% |

$ |

29,715 |

|

$ |

923 |

|

3.12 |

% | ||

|

Real

estate construction loans |

2,508 |

|

91 |

|

3.63 |

|

1,884 |

|

66 |

|

3.48 |

|

1,909 |

|

65 |

|

3.41 |

| ||||||||

|

Commercial

mortgage loans |

8,981 |

|

314 |

|

3.49 |

|

8,697 |

|

296 |

|

3.41 |

|

8,706 |

|

327 |

|

3.75 |

| ||||||||

|

Lease

financing |

684 |

|

18 |

|

2.65 |

|

783 |

|

25 |

|

3.17 |

|

834 |

|

19 |

|

2.33 |

| ||||||||

|

International

loans |

1,367 |

|

50 |

|

3.63 |

|

1,441 |

|

51 |

|

3.58 |

|

1,376 |

|

50 |

|

3.65 |

| ||||||||

|

Residential

mortgage loans |

1,894 |

|

71 |

|

3.76 |

|

1,878 |

|

71 |

|

3.77 |

|

1,778 |

|

68 |

|

3.82 |

| ||||||||

|

Consumer

loans |

2,500 |

|

83 |

|

3.32 |

|

2,444 |

|

80 |

|

3.26 |

|

2,270 |

|

73 |

|

3.20 |

| ||||||||

|

Total

loans (b) (c) |

48,996 |

|

1,635 |

|

3.34 |

|

48,628 |

|

1,551 |

|

3.20 |

|

46,588 |

|

1,525 |

|

3.28 |

| ||||||||

|

Mortgage-backed

securities |

9,356 |

|

203 |

|

2.19 |

|

9,113 |

|

202 |

|

2.24 |

|

8,970 |

|

209 |

|

2.33 |

| ||||||||

|

Other

investment securities |

2,992 |

|

44 |

|

1.51 |

|

1,124 |

|

14 |

|

1.25 |

|

380 |

|

2 |

|

0.45 |

| ||||||||

|

Total

investment securities (d) |

12,348 |

|

247 |

|

2.02 |

|

10,237 |

|

216 |

|

2.13 |

|

9,350 |

|

211 |

|

2.26 |

| ||||||||

|

Interest-bearing

deposits with banks |

5,099 |

|

26 |

|

0.51 |

|

6,158 |

|

16 |

|

0.26 |

|

5,513 |

|

14 |

|

0.26 |

| ||||||||

|

Other

short-term investments |

102 |

|

1 |

|

0.61 |

|

106 |

|

1 |

|

0.81 |

|

109 |

|

— |

|

0.57 |

| ||||||||

|

Total

earning assets |

66,545 |

|

1,909 |

|

2.88 |

|

65,129 |

|

1,784 |

|

2.75 |

|

61,560 |

|

1,750 |

|

2.85 |

| ||||||||

|

Cash

and due from banks |

1,146 |

|

1,059 |

|

934 |

|

||||||||||||||||||||

|

Allowance

for loan losses |

(730 |

) |

(621 |

) |

(601 |

) |

||||||||||||||||||||

|

Accrued

income and other assets |

4,782 |

|

4,680 |

|

4,443 |

|

||||||||||||||||||||

|

Total

assets |

$ |

71,743 |

|

$ |

70,247 |

|

$ |

66,336 |

|

|||||||||||||||||

|

Money

market and interest-bearing checking deposits |

$ |

22,744 |

|

27 |

|

0.11 |

|

$ |

24,073 |

|

26 |

|

0.11 |

|

$ |

22,891 |

|

24 |

|

0.11 |

| |||||

|

Savings

deposits |

2,013 |

|

— |

|

0.02 |

|

1,841 |

|

— |

|

0.02 |

|

1,744 |

|

1 |

|

0.03 |

| ||||||||

|

Customer

certificates of deposit |

3,200 |

|

13 |

|

0.40 |

|

4,209 |

|

16 |

|

0.37 |

|

4,869 |

|

18 |

|

0.36 |

| ||||||||

|

Foreign

office time deposits (e) |

33 |

|

— |

|

0.35 |

|

116 |

|

1 |

|

1.02 |

|

261 |

|

2 |

|

0.82 |

| ||||||||

|

Total

interest-bearing deposits |

27,990 |

|

40 |

|

0.14 |

|

30,239 |

|

43 |

|

0.14 |

|

29,765 |

|

45 |

|

0.15 |

| ||||||||

|

Short-term

borrowings |

138 |

|

— |

|

0.45 |

|

93 |

|

— |

|

0.05 |

|

200 |

|

— |

|

0.04 |

| ||||||||

|

Medium-

and long-term debt (f) |

4,917 |

|

72 |

|

1.45 |

|

2,905 |

|

52 |

|

1.80 |

|

2,963 |

|

50 |

|

1.68 |

| ||||||||

|

Total

interest-bearing sources |

33,045 |

|

112 |

|

0.34 |

|

33,237 |

|

95 |

|

0.29 |

|

32,928 |

|

95 |

|

0.29 |

| ||||||||

|

Noninterest-bearing

deposits |

29,751 |

|

28,087 |

|

25,019 |

|

||||||||||||||||||||

|

Accrued

expenses and other liabilities |

1,273 |

|

1,389 |

|

1,016 |

|

||||||||||||||||||||

|

Total

shareholders’ equity |

7,674 |

|

7,534 |

|

7,373 |

|

||||||||||||||||||||

|

Total

liabilities and shareholders’ equity |

$ |

71,743 |

|

$ |

70,247 |

|

$ |

66,336 |

|

|||||||||||||||||

|

Net

interest income/rate spread |

$ |

1,797 |

|

2.54 |

|

$ |

1,689 |

|

2.46 |

|

$ |

1,655 |

|

2.56 |

| |||||||||||

|

Impact

of net noninterest-bearing sources of funds |

|

0.17 |

|

0.14 |

|

0.14 |

| |||||||||||||||||||

|

Net interest margin (as a

percentage of average earning assets) (b) (d) |

|

|

2.71 |

% |

|

|

2.60 |

% |

|

|

2.70 |

% | ||||||||||||||

|

(a) |

Average

rate is calculated on a fully taxable equivalent (FTE) basis using a

federal tax rate of 35%. The FTE adjustment to net interest income was $4

million in each of the three years

presented. |

|

(b) |

Accretion

of the purchase discount on the acquired loan portfolio of $4

million,

$7

million

and $34

million

in 2016,

2015 and

2014,

respectively, increased the net interest margin by 1 basis

point in both 2016 and

2015 and

6 basis

points in 2014. |

|

(c) |

Nonaccrual

loans are included in average balances reported and in the calculation of

average rates. |

|

(d) |

Includes

investment securities available-for-sale and investment securities

held-to-maturity. Average rate based on average historical cost. Carrying

value exceeded average historical cost by

$143

million,

$100

million

and $12

million

in 2016,

2015 and

2014,

respectively. |

|

(e) |

Includes

substantially all deposits by foreign depositors; deposits are primarily

in excess of $100,000. |

|

(f) |

Medium-

and long-term debt average balances included $162

million,

$160

million

and $192

million

in 2016,

2015 and

2014,

respectively, for the gain attributed to the risk hedged with interest

rate swaps. Interest expense on medium-and long-term debt was reduced by

$60

million,

$70

million,

and $72

million

in 2016,

2015 and

2014,

respectively, for the net gains on these fair value hedge

relationships. |

|

(in

millions) |

|||||||||||||||||||||||||

|

Years

Ended December 31 |

2016/2015 |

2015/2014 | |||||||||||||||||||||||

|

Increase

(Decrease)

Due to Rate |

Increase

(Decrease)

Due to

Volume (a) |

Net

Increase

(Decrease) |

Increase

(Decrease)

Due to Rate |

Increase

(Decrease)

Due to

Volume (a) |

Net

Increase

(Decrease) | ||||||||||||||||||||

|

Interest

Income: |

|||||||||||||||||||||||||

|

Commercial

loans |

$ |

60 |

|

$ |

(14 |

) |

$ |

46 |

|

$ |

(15 |

) |

$ |

54 |

|

$ |

39 |

|

|||||||

|

Real

estate construction loans |

2 |

|

23 |

|

25 |

|

2 |

|

(1 |

) |

1 |

|

|||||||||||||

|

Commercial

mortgage loans |

8 |

|

10 |

|

18 |

|

(31 |

) |

— |

|

(31 |

) |

|||||||||||||

|

Lease

financing |

(4 |

) |

(3 |

) |

(7 |

) |

8 |

|

(2 |

) |

6 |

|

|||||||||||||

|

International

loans |

1 |

|

(2 |

) |

(1 |

) |

(1 |

) |

2 |

|

1 |

|

|||||||||||||

|

Residential

mortgage loans |

— |

|

— |

|

— |

|

(1 |

) |

4 |

|

3 |

|

|||||||||||||

|

Consumer

loans |

1 |

|

2 |

|

3 |

|

1 |

|

6 |

|

7 |

|

|||||||||||||

|

Total

loans |

68 |

|

16 |

|

84 |

|

(37 |

) |

(b) |

63 |

|

26 |

|

(b) | |||||||||||

|

Mortgage-backed

securities |

(4 |

) |

5 |

|

1 |

|

(8 |

) |

1 |

|

(7 |

) |

|||||||||||||

|

Other

investment securities |

3 |

|

27 |

|

30 |

|

3 |

|

9 |

|

12 |

|

|||||||||||||

|

Total

investment securities (c) |

(1 |

) |

32 |

|

31 |

|

(5 |

) |

10 |

|

5 |

|

|||||||||||||

|

Interest-bearing

deposits with banks |

15 |

|

(5 |

) |

10 |

|

— |

|

2 |

|

2 |

|

|||||||||||||

|

Other

short-term investments |

— |

|

— |

|

— |

|

— |

|

1 |

|

1 |

|

|||||||||||||

|

Total

interest income |

82 |

|

43 |

|

125 |

|

(42 |

) |

76 |

|

34 |

|

|||||||||||||

|

Interest

Expense: |

|||||||||||||||||||||||||

|

Money

market and interest-bearing checking deposits |

2 |

|

(1 |

) |

1 |

|

— |

|

2 |

|

2 |

|

|||||||||||||

|

Savings

deposits |

— |

|

— |

|

— |

|

(1 |

) |

— |

|

(1 |

) |

|||||||||||||

|

Customer

certificates of deposit |

1 |

|

(4 |

) |

(3 |

) |

1 |

|

(3 |

) |

(2 |

) |

|||||||||||||

|

Foreign

office time deposits |

(1 |

) |

— |

|

(1 |

) |

1 |

|

(2 |

) |

(1 |

) |

|||||||||||||

|

Total

interest-bearing deposits |

2 |

|

(5 |

) |

(3 |

) |

1 |

|

(3 |

) |

(2 |

) |

|||||||||||||

|

Medium-

and long-term debt |

9 |

|

11 |

|

20 |

|

3 |

|

(1 |

) |

2 |

|

|||||||||||||

|

Total

interest expense |

11 |

|

6 |

|

17 |

|

4 |

|

(4 |

) |

— |

|

|||||||||||||

|

Net

interest income |

$ |

71 |

|

$ |

37 |

|

$ |

108 |

|

$ |

(46 |

) |

$ |

80 |

|

$ |

34 |

|

|||||||

|

(a) |

Rate/volume

variances are allocated to variances due to

volume. |

|

(b) |

Reflected

a decrease of $27

million

in accretion of the purchase discount on the acquired loan portfolio in

2015. |

|

(c) |

Includes

investment securities available-for-sale and investment securities

held-to-maturity. |

|

(in

millions) |

||||||||||||

|

Years

Ended December 31 |

2016 |

2015 |

2014 | |||||||||

|

Card

fees |

$ |

303 |

|

(a) |

$ |

276 |

|

(a) |

$ |

81 |

|

|

|

Service

charges on deposit accounts |

219 |

|

223 |

|

215 |

|

||||||

|

Fiduciary

income |

190 |

|

187 |

|

180 |

|

||||||

|

Commercial

lending fees |

89 |

|

99 |

|

98 |

|

||||||

|

Letter

of credit fees |

50 |

|

53 |

|

57 |

|

||||||

|

Bank-owned

life insurance |

42 |

|

40 |

|

39 |

|

||||||

|

Foreign

exchange income |

42 |

|

40 |

|

40 |

|

||||||

|

Brokerage

fees |

19 |

|

17 |

|

17 |

|

||||||

|

Net

securities losses |

(5 |

) |

(2 |

) |

— |

|

||||||

|

Other

noninterest income (b) |

102 |

|

102 |

|

130 |

|

||||||

|

Total

noninterest income |

$ |

1,051 |

|

$ |

1,035 |

|

$ |

857 |

|

|||

|

(a) |

Effective

January 1, 2015, contractual changes to a card program resulted in a

change to the accounting presentation of the related revenues and

expenses. The effect of this change was an increase to card fees of $182

million in 2016 and $177 million in 2015. |

|

(b) |

The

table below provides further details on certain categories included in

other noninterest income. |

|

(in

millions) |

|||||||||||||

|

Years

Ended December 31 |

2016 |

2015 |

2014 | ||||||||||

|

Customer

derivative income |

$ |

27 |

|

$ |

18 |

|

$ |

22 |

|

||||

|

Insurance

commissions |

10 |

|

10 |

|

13 |

|

|||||||

|

Investment

banking fees |

7 |

|

12 |

|

18 |

|

|||||||

|

Income

from principal investing and warrants |

7 |

|

6 |

|

10 |

|

|||||||

|

Securities

trading income |

6 |

|

9 |

|

9 |

|

|||||||

|

Deferred

compensation asset returns (a) |

3 |

|

— |

|

6 |

|

|||||||

|

Income

from unconsolidated subsidiaries |

(2 |

) |

2 |

|

8 |

|

|||||||

|

All

other noninterest income |

44 |

|

45 |

|

44 |

|

|||||||

|

Other

noninterest income |

$ |

102 |

|

$ |

102 |

|

$ |

130 |

|

||||

|

(a) |

Compensation

deferred by the Corporation's officers and directors is invested based on

investment selections of the officers and directors. Income earned on

these assets is reported in noninterest income and the offsetting change

in liability is reported in salaries and benefits

expense. |

|

(in

millions) |

||||||||||||

|

Years

Ended December 31 |

2016 |

2015 |

2014 | |||||||||

|

Salaries

and benefits expense |

$ |

961 |

|

$ |

1,009 |

|

$ |

980 |

|

|||

|

Outside

processing fee expense |

336 |

|

(a) |

318 |

|

(a) |

111 |

|

||||

|

Net

occupancy expense |

157 |

|

159 |

|

171 |

|

||||||

|

Equipment

expense |

53 |

|

53 |

|

57 |

|

||||||

|

Restructuring

expense |

93 |

|

— |

|

— |

|