Mid-Year Media Review

New York

June 18, 2002

Donald

E. Graham

Chairman of the Board and Chief Executive Officer

Good morning. In past years we’ve used this occasion to give you a quick review of our progress year-to-date. We’ll do that today, but I’d also like to step back for a moment. The path our company has been on for the past several years is so different from that of most companies you follow, I thought it would be helpful to talk about what we’ve set out to do, and how well we’re meeting our objectives.

When I first spoke to this group as CEO of The Washington Post Company 11 years ago, I said we would do two things to build the value of the company. First, we would run our operating businesses well.

Second, we would make prudent use of our shareholders’ money by making acquisitions with the aim of growing value. By value, we mean building businesses capable of sustained growth in operating income over the long term.

This morning, I’d like to focus on the second part of that agenda, by describing the growth and future prospects of Cable ONE and Kaplan, which have been the targets of our greatest investment activity in the past few years.

I’ll start with Cable ONE; you could call this presentation “Building Shareholder Value the Old Fashioned Way.”

We acquired our cable business in 1986 with the $350 million acquisition of 350,000 cable subscribers from Cap Cities.

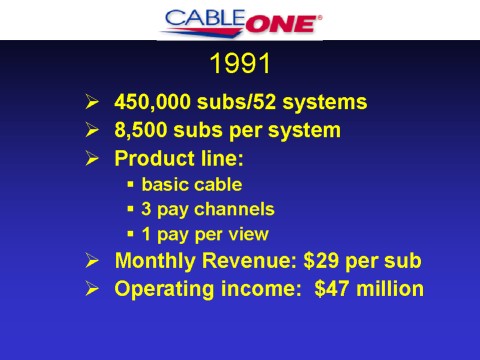

By the time I took over in 1991, the cable operation looked like this: We had 450,000 subs in 52 systems across the country. We had a product line consisting of basic cable, 3 pay channels, and 1 pay-per-view that was generating $29 monthly revenue per sub. Operating income, excluding amortization totaled $47 million, with free cash flow of $100 per sub. Then, under Tom Might’s leadership, Cable ONE began to manage the operation in a unique way, far different from any other MSO.

First, of course, we made the decision to stay in the business.

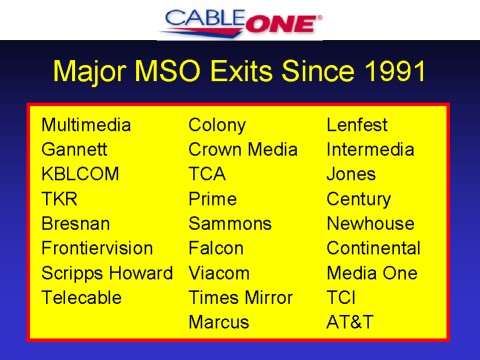

Here are MSO owners who chose to sell or merge since 1991, understandably, because of the rising prices acquirers were willing to pay. We decided to stay in the business – after a careful review with our Board – because we believed our management is very good and because we liked the kind of system we were primarily in.

For the most part, we were in small-city, non-metro markets. That has spared us the high capital expense of building in urban environments and the high acquisition costs of acquiring high-demo subscribers. As a result, we never generate the revenue per subscriber of the best-run urban systems. But we avoid the capital and competitive demands of all urban systems.

Our second decision was to grow our subscriber base and concentrate our systems even further in the most efficient way possible.

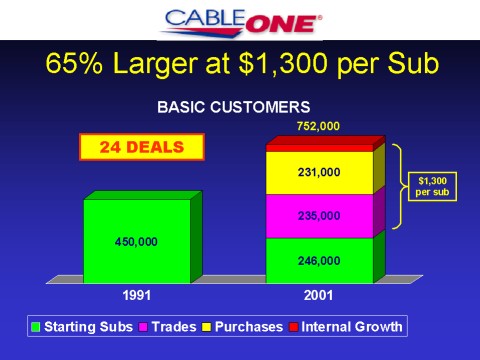

500,000 of our subscribers were new to Cable ONE in the past decade, thanks to 24 deals, many of which you probably never read about in Multichannel News. We made a series of trades where we gave up more than 200,000 of our original subscribers that did not fit our operating and geographical strategies, and gained 235,000 that did. In addition, we purchased over 200,000 more outright.

There’s another thing that makes Cable ONE unique: We don’t like paying $5,000 per sub in acquisitions, nor $4,000, nor even $3,000. We have paid a little more than $2,000 on a few occasions. Our net cost has only been $1,300 per new subscriber.

When Paul Allen entered the market in 1997 and prices went up so dramatically, we stepped aside for a few years to wait for better deals.

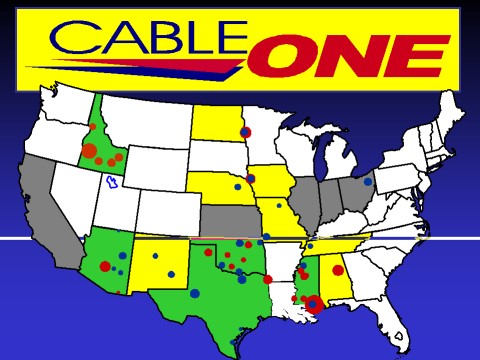

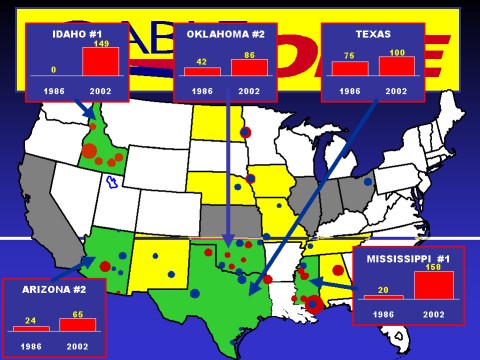

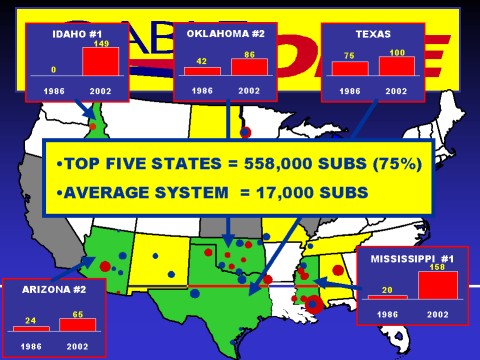

Here is the resulting Cable ONE map. All the red dots are new to Cable ONE in the past decade. The gray states are those we have exited or will exit soon. The green states are those in which we’ve grown to a significant presence.

In Mississippi and Idaho we came from nowhere to first in the state. In Arizona and Oklahoma we came from nowhere to second-largest MSO in the state.

These four states, plus Texas, contain 75 percent of all Cable ONE subscribers, and the average system size has doubled to 17,000 subs per system.

In fact, we have fewer headends today, with three-quarters of a million

subscribers, than we had when we entered cable in 1986, with 350,000 subscribers.

That bodes well for the economics of launching new services, such as digital

cable and cable modems.

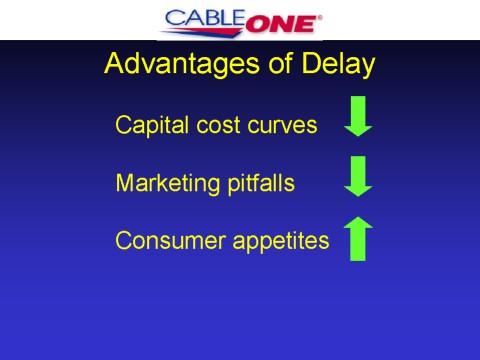

Our third decision was to make Cable ONE the last, or next-to-last, major MSO to introduce each of these services. By operating outside metro markets, we can wait for technology and products to ripen before introducing them to customers.

By then, capital cost curves have been driven down by others, marketing pitfalls have been exposed by others, and consumer appetites have been piqued by others.

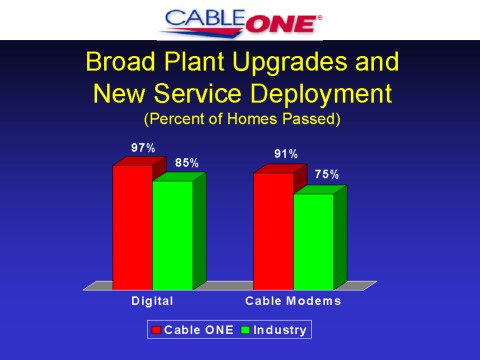

Less than two years after we started, more than 90 percent of our customers are now offered digital and cable modem services.

Just to remind you, we gave digital away free for 12 months to any interested customer, most of whom agreed to do a cost-saving self-installation in return. And we were the only MSO to launch without @Home or another ISP partner, with which we would have had to share revenues.

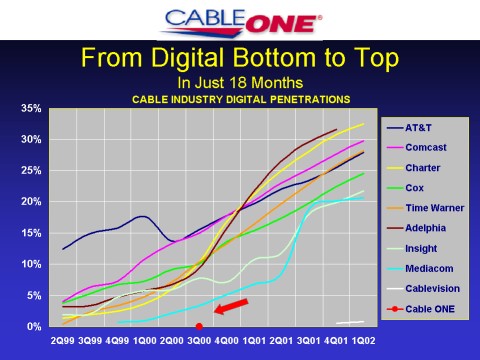

Here we see the quarterly digital penetration of the top ten MSOs going back three years or more – with Adelphia and Charter taking the lead positions in 2001. Notice the red dot at the bottom. That is Cable ONE’s launch, less than two years ago.

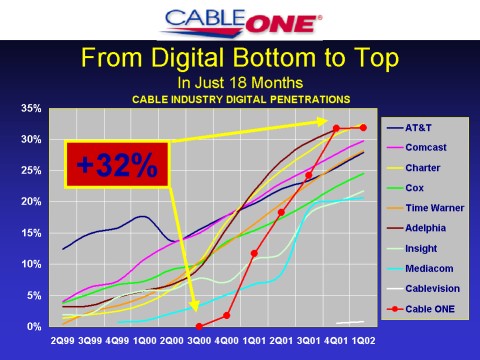

And

here is the rest of the story. By

the end of 2001, just 18 months after launch, we had passed all nine

other MSOs. Benefiting from

the lessons of others, we chose unique technology and the radical

“free 12-month” marketing tactic – now expired – to break out of

the digital mold.

Recently the question has been, “Will it stick when they have to pay for it?” For those subs that took the free offer for the full 12 months, the initial conversion rate was in excess of 90 percent. As you can see, Cable ONE has held on to 32 percent penetration through the first quarter – in fact, through April and May as well.

That figure will slip, but we will end the year with higher digital penetration than we could possibly have obtained through a traditional digital rollout.

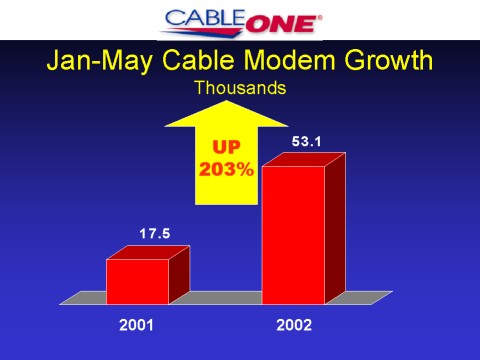

Cable modem subscriber growth has been equally strong, up 203 percent through May. Today we have more than 53,000 modem customers. Since Cable ONE was the last major MSO to launch modems, it lags the industry in penetration, with just 8 percent to date, including modem and dial-up customers.

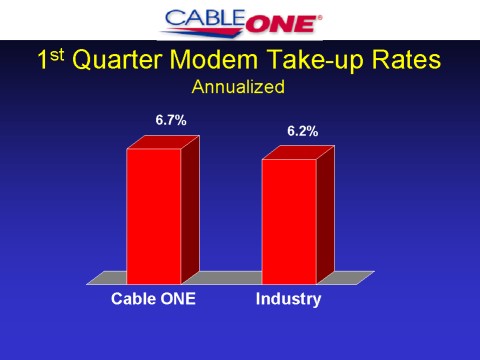

But, we’re now enjoying the robust national demand for cable modems – growing at an annualized rate of 6.7 percent of subscribers in the first quarter, slightly ahead of the industry average. Margins are particularly good because of the absence of an ISP partner.

The deployment of these new services is a major factor in the solid year Cable ONE is now enjoying.

Year-to-date, cash flow has been running at a rate of 22 percent above last year. We’ve achieved that growth by selling new services more efficiently, not by increasing the number of subscribers. At the end of May, we had about 744,000 subs. That’s actually down about 2.5 percent, from a year earlier.

Over that 12-month period we had no acquisitions. The decline reflects the competitive pressure from satellite and perhaps even more, the pressure of a down economy. We doubled the number of disconnects for non-payment against the prior year.

At this point it’s impossible to predict what will happen to subscriber counts going forward. With continuing competitive pressure from DBS and an uncertain economy, I wouldn’t be at all surprised if the erosion we’ve seen in the last 12 months were to continue. We’re budgeting and planning cautiously.

The picture wouldn’t be complete without a discussion of capital spending, because all of this growth in the cable business comes at a substantial capital

cost.

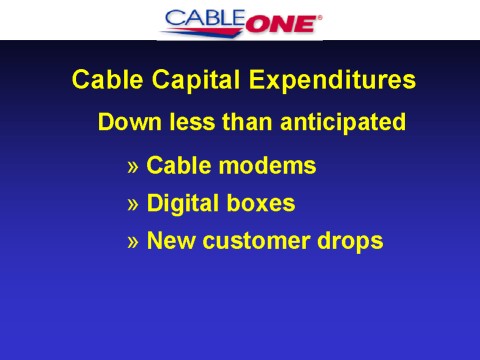

Fortunately, we got most of the needed capital spending behind us in 2001. But we are still spending at a substantial rate this year – in fact, at a higher rate than I had hoped for. We had anticipated that capital spending in 2002 would be as much as $100 million less than in 2001. As the year is developing, the fall-off is somewhat less than I had hoped, but we still expect to end the year spending about $70 million less than in 2001.

We’re spending at a higher than expected rate this year for several reasons.

First, cable modem growth has been much faster than we expected.

Second, we bought and are deploying more digital boxes than we had originally forecast. Although the number of digital subscribers is less than we had optimistically hoped for, the number of boxes per household is greater. Fully 28 percent of the homes have more than one box, which at $4.95 for each additional box means higher revenue for us.

Third, the migration to digital has required capital spending in some areas that we did not adequately anticipate. For example, we substantially underestimated the number of new customer drops that would be needed to facilitate two-way communication. When this is all done, we will have installed three to four times as many new customer drops as we had initially projected.

Our rate of capital spending per subscriber is still at industry-low levels.

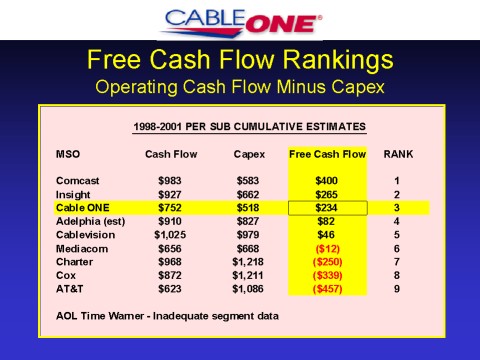

Here’s a look at free cash flow: Even with Cable ONE’s plant upgraded and new services launched – we spent $248 million in 2000 and 2001 – we have the lowest capital spending per sub in the industry, which more than compensates for our slightly lower operating cash flow. The origin of this data is an article Rich Bilotti of Morgan Stanley Dean Witter wrote two years ago, entitled “Grading the MSOs.” We have added to his work as accurately as possible each year since then, based on publicly disclosed data.

This slide tells the story through 2001, but there’s no reason to think that adding in 2002 results would change the picture. We expect average capital spending per sub this year of approximately $130, down more than 40 percent from $222 last year. By contrast, the industry average, judging by the data we’ve seen, is running at a rate of about $212 – in other words, about $82 more per sub than Cable ONE.

So here’s how our goal of building value in Cable ONE has turned out. Over the past decade, we’ve added another 300,000 subscribers at rock bottom prices, adding a lot of value for our shareholders. We expect substantial growth in free cash this year.

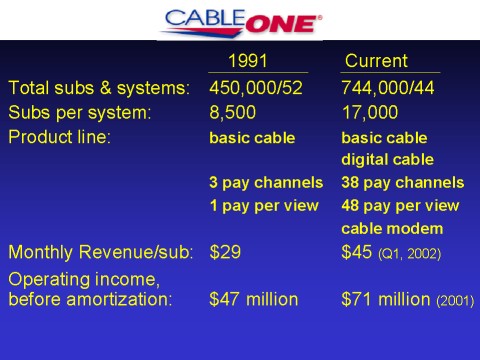

To remind you, here’s where we stand today versus 1991. We’ve concentrated 744,000 subs in 44 systems. We’ve increased our product line to include digital and cable modem. Our monthly revenue for the first quarter of 2002 was roughly $45 per sub. Despite being hammered by the Idaho trade and increased depreciation expense from heavy capital spending, operating income in 2001 was $71 million, excluding amortization. We like our prospects for revenue and operating income growth for 2002 and beyond.

We’ve also built value at Kaplan. In fact, we believe Kaplan may present a larger growth opportunity in the long term than Cable ONE, especially as cable acquisition prices have gone sky high in recent years. Because of the fragmented nature of the education business – and because Kaplan is active in many parts of it – we have been able to find more attractive acquisition opportunities up to now.

It’s harder to quantify Kaplan’s increasing value, because it’s not simply a question of, say, multiplying the number of cable subscribers by the price per sub. Nonetheless, the growth has been real – and substantial.

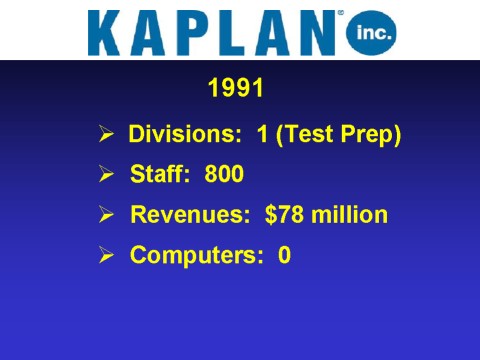

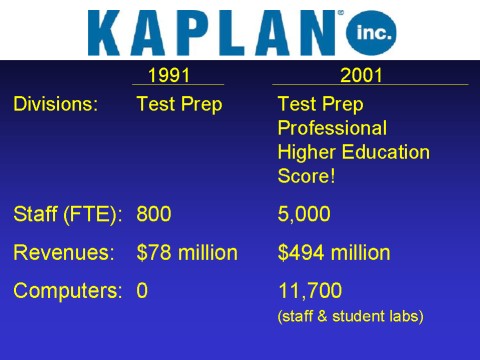

Here’s what Kaplan looked like in 1991, when I first spoke to this group. As you can see, the company consisted of a single operation: the original Test Prep business Stanley Kaplan invented in his Brooklyn basement in 1938. The company had a staff of 800, less than $80 million in revenues, and quite alarmingly, profitability had started to decline precipitously.

Kaplan had been profitable when we acquired it in 1984, but the advent of a feisty competitor and the difficulties of managing a contractor-based work force had sapped Kaplan’s earnings. And to show you just how “primitive” the education business was a mere decade ago, Kaplan had no computers in its centers!

Once again, we began to build the business.

First, in 1992, we installed a new management team led by Jonathan Grayer, whose managerial excellence and financial sense have made all the difference. Jonathan and his team – a team led by Andy Rosen, who just became Kaplan’s president – began to transform this business. To begin with, they brought Kaplan’s work force in-house, making formerly independent contractors Kaplan employees.

This gave us the structure to drive the original business forward, making a variety of improvements. Then they began a pretty big acquisition program that has taken Kaplan into a range of education businesses that serve people from elementary school to the end of their professional lives.

In the long run, the best way to understand Kaplan is to study each of its operating divisions, but I admit this takes some doing.

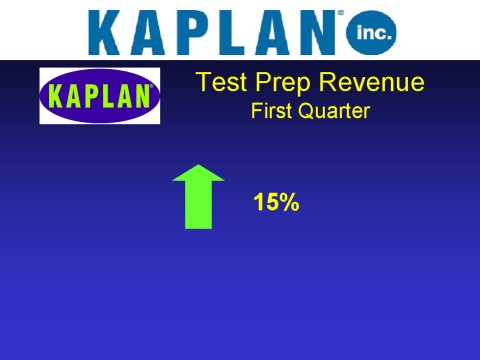

Kaplan Test Prep, the original business, is thriving. We continue to take market share from competitors. As we reported, revenues were up 15 percent in the first quarter of 2002 – this growth has continued into the second quarter.

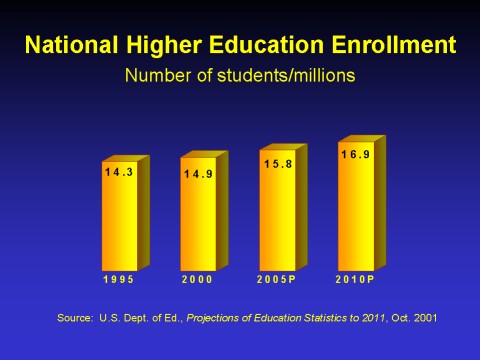

Our courses are growing steadily and should continue to grow as 2 million more students are projected to go to college as well as to law, business, and other graduate programs by the end of this decade. Graduate school enrollments have increased since the dot.com bust.

Kaplan Professional is a business that has been built entirely through acquisitions – some 13 acquisitions for a total of $117 million over the past four years. Revenue for Kaplan Professional grew 4 percent in the first quarter, despite obvious softness in the securities and IT training areas – both of which continue to be among Kaplan Professional’s largest markets.

Meanwhile, its real estate training and publishing businesses are booming. Before acquisitions – primarily Prosource – total real estate revenue increased 46 percent in the first quarter, and operating income increased 131 percent. Including Prosource, revenues were up by 116 percent and profitability was up 261 percent in the first quarter. Kaplan’s CFA business also continues very strong.

The results at Score after-school educational centers for kids in grades K through 10 continue to improve. Students have begun staying for longer periods of time, and revenue per student has grown. As a result, losses in this operation are shrinking.

One of the most exciting areas for growth at Kaplan has been its post-secondary education business, where enrollments continue to grow. Kaplan’s Higher Education division has both campus-based and online offerings.

The business has been built through a series

of acquisitions, highlighted by the acquisition of Quest for $178

million in 2000.

Since then, Kaplan has continued to add

colleges at decent prices. Last

month Kaplan announced it had acquired Tesst, a fine group of four

bricks-and-mortar colleges in Maryland and Virginia.

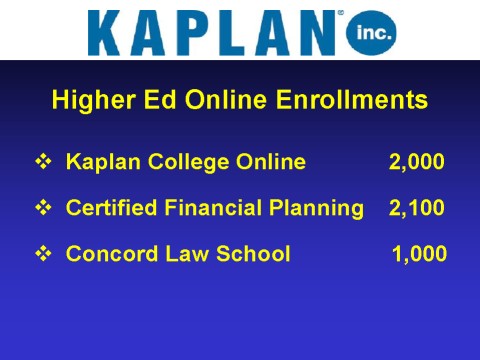

Kaplan’s online schools look promising, too, as we’re enrolling and retaining more students, and losses are coming down.

For the first quarter, Higher Ed’s online

schools had nearly 2,000 students in its degree programs, and more than

2,100 in its Certified Financial Planning programs.

Concord Law School has 1,000 active students.

It is now profitable and will graduate its first class of

students this fall.

Barry Diller will be the commencement

speaker. Take that, Harvard

Law School!

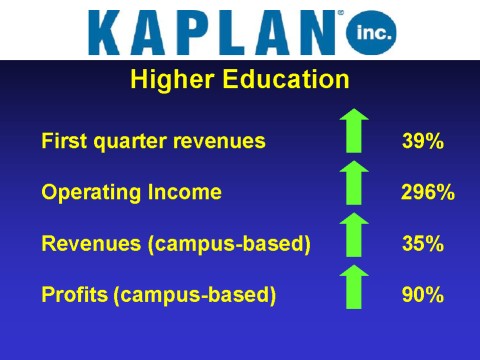

First quarter revenues were up 39 percent

– which includes some acquisitions – and operating income was up

nearly 300 percent, albeit off a small base.

Revenues for campus-based programs alone were up 35 percent, with

profits up 90 percent.

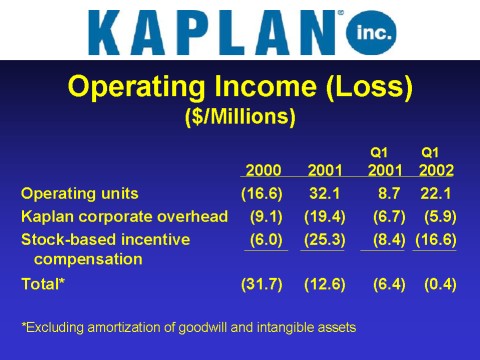

On a consolidated basis, here are Kaplan’s

recent results. Kaplan’s

operating units went from a loss of $16.6 million in 2000, to a profit

of $32.1 million in 2001. Continuing

the trend in the first quarter of 2002, Kaplan’s operating units

generated profits of $22.1 million, compared to $8.7 million in 2001.

Here’s how Kaplan today stacks up against

the Kaplan of 1991. I wish

I could give you a metric model to plug in Kaplan’s results and

establish the company’s value. I

cannot.

As Kaplan’s value increases, so too do our

accruals for Kaplan’s management compensation plan, which is a major

factor in the overall Kaplan results we report to the public.

This plan resembles a stock-option plan, although the accounting

is quite different.

To date, the plan has been virtually all

non-cash, but we absolutely expect to pay out cash in the future.

This year’s accrual will be significantly larger than in 2001.

So today, accruals are being booked, but no

cash is being paid out; in the future, the accruals may lessen, but the

cash will be paid. Kaplan’s value for purposes of this plan is set by the

Compensation Committee of our Board of Directors.

They factor in Kaplan’s results, the valuations of public

companies in the field, and input from an independent outside firm.

What began as a $40 million acquisition of Stanley’s original business has skyrocketed through internal growth and $380 million in acquisitions into a company worth considerably more than what we have in it.

Another focus of our investment spending has been Washingtonpost.Newsweek Interactive. In key respects our progress has been good.

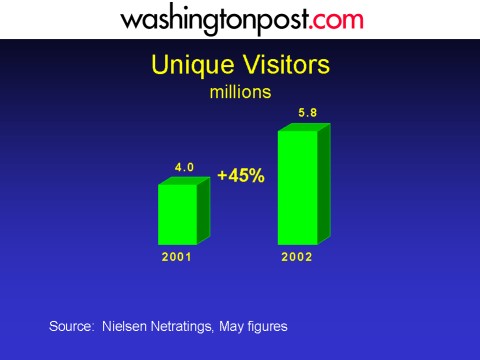

washingtonpost.com continues to see dramatic

growth in traffic to the site. The

latest figures from Nielsen Netratings show 5.8 million unique visitors

in May, up 45 percent compared to May 2001.

These figures come as washingtonpost.com continues to expand its national and international audience. About 80 percent of the site’s traffic comes from outside the Washington, DC area. And while the site’s national audience is on a steady climb, the site has continued to dominate the DC market.

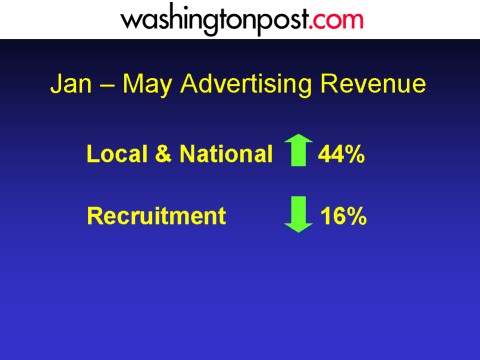

In terms of advertising, it’s a tale of

two cities. Local and national advertising across the site is growing,

driven by a series of new ad products.

Right now, these ad revenues are up 44 percent through May.

The net result: Total revenue for the year

is up 3 percent versus 2001.

We continue to be optimistic that this

business will pay off for our shareholders over the long term.

But it will take some time.

Although I’ve been focusing on building value through acquisitions and investments, I don’t want to neglect the importance of our second objective: to operate our traditional ad-based businesses well. I believe our managers are continuing to do a good job in a very difficult environment.

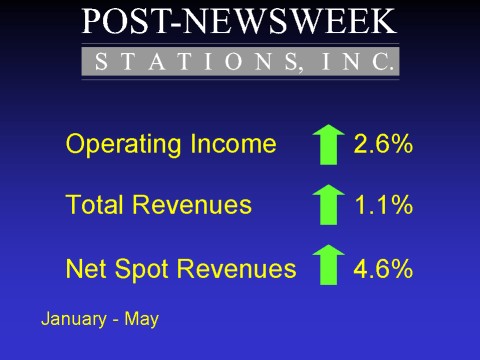

Post-Newsweek Stations is having a pretty good year.

Operating income in the first five months

was up 2.6 percent. And despite a drop in network compensation, total revenues

advanced 1.1 percent. Net

spot revenues grew 4.6 percent. Year-to-date

spot revenue increases are outpacing industry averages.

Our two largest stations, WDIV in Detroit and KPRC in Houston, carried the Winter Olympics from Salt Lake City in February. As usual, the Olympics generated significant, non-recurring incremental revenues, of $4.9 million net. The combined revenues of our non-Olympics stations were up slightly through the first five months of the year, as expected.

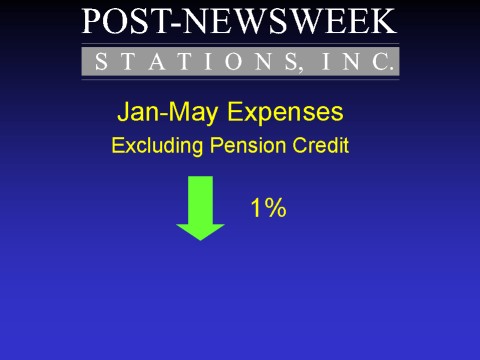

In a tight advertising climate, expense control is always a priority. At Post-Newsweek, expenses in the first five months were down 1 percent compared to 2001, excluding the pension credit. Expenses for full year 2002 will end up slightly less than in 1998.

In early April we announced that WJXT in

Jacksonville would not be renewing its 50-plus-year affiliation with

CBS. The change will take

place on July 15.

It pains me to see WJXT’s relationship

with CBS end. The relationship has always been a good one for both sides.

I should add that Mel Karmazin and Les Moonves were thoroughly

professional in their dealing with us throughout the negotiations, in

the tradition of their excellent network.

For more than two years, we attempted to

come to an agreement with CBS. These

efforts were unsuccessful. After

a very careful analysis of our options, we decided the long-term best

interest of the station – and the company – would be served by going

independent, although we expect our margins to suffer in the short term.

Local news and local public affairs programs

on WJXT are among the most successful in the nation.

The station will build on this foundation by almost doubling the

number of hours of news it produces each week.

We have made a substantial investment to ensure WJXT has the

resources it needs for the transition.

The related start-up costs, increased staff, and additional

program costs will cause a significant increase in expenses over the

next 18 months.

However, on the revenue side, because of WJXT’s exceptionally strong local presence and because of the additional spot inventories of an independent, we expect the station’s revenues will continue to grow long-term.

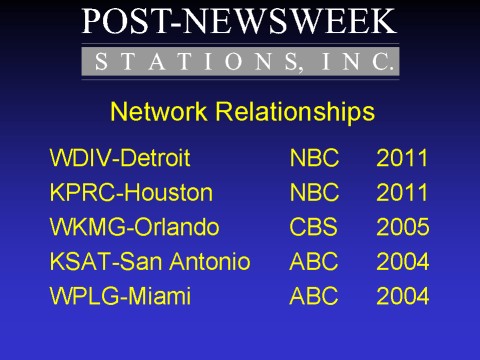

As for our relationship with the other networks, we have renewed our affiliate contract with NBC for our stations in Detroit and Houston through 2011. Our network agreement with CBS for Orlando expires in 2005, and our agreements with ABC for San Antonio and Miami expire at the end of 2004.

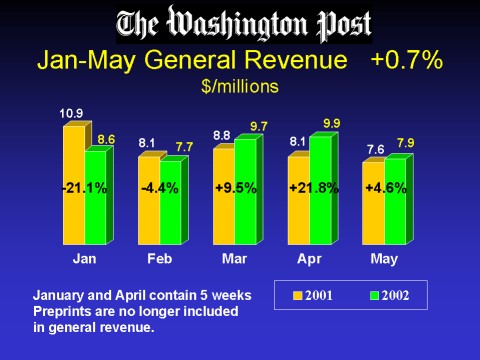

The Washington Post newspaper is still

suffering from the Recession Blues we talked about last year.

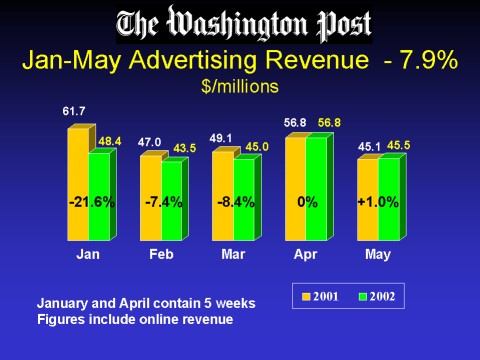

Through May, ad revenue was off 7.9 percent.

The declines were steepest in January (21.6 percent), with the

following months off in the 7-to-8 percent range.

Note that April was flat with last year. This is somewhat misleading.

Much of the improvement has to do with the timing of Easter –

April last year and March this year.

May was up 1 percent over last year, which is encouraging, but it

is far too early to conclude that we’ve either hit or bounced off the

bottom.

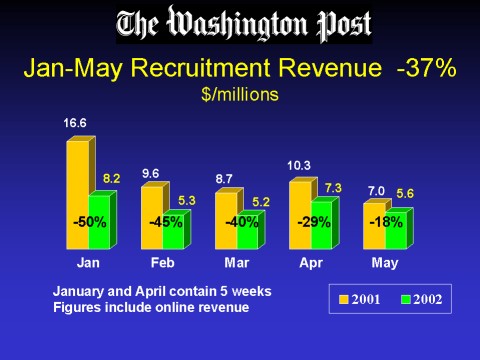

As you will be hearing again and again, much of the advertising falloff is in the recruitment category.

Through May, recruitment was off 37 percent from last year. The recruitment trend is improving as the year progresses.

Other advertising categories are not faring as badly. Retail is off 10.5 percent through May. This slide shows the month-by-month breakdown. As you can see, we had our best performance in May, although we’re still down.

General advertising has grown in March,

April, and May. Year-to-date we’re slightly ahead of last year.

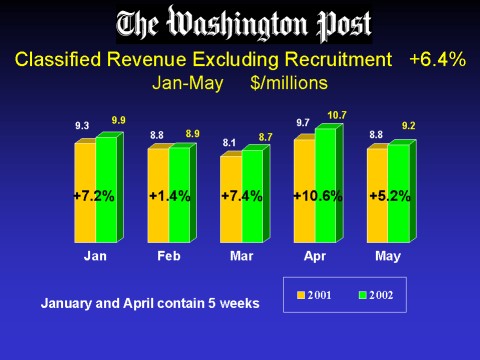

The non-recruitment side of classified has showed gratifying growth this year, fueled by automotive and real estate. This segment is up 6.4 percent through May.

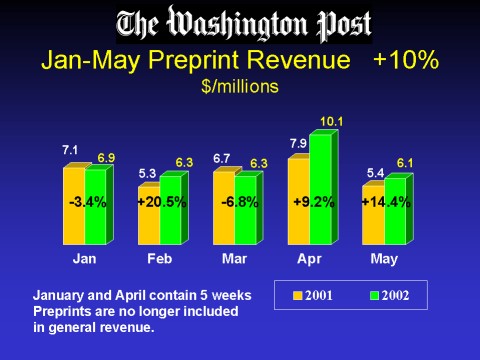

Preprint advertising, an important portion

of our business that is susceptible to raids from direct mail, is up by

10 percent. As you can see,

however, this business has had its ups and downs.

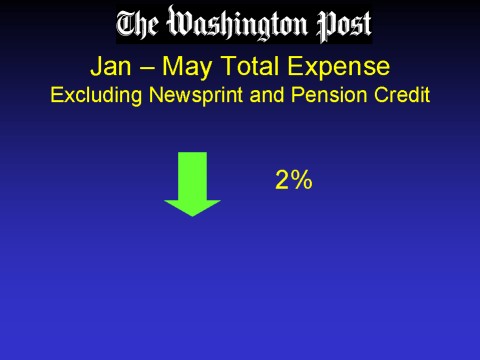

As you know, The Post has always managed expenses closely in good times and manages them even more closely, if possible, during the bad. Like others, we’ve been helped by softness in the newsprint market, and fewer ads means fewer pages to run.

As a result, newsprint expense is down by 25 percent over last year.

By carefully managing departmental operating

expenses and headcount, total expenses at the newspaper, excluding

newsprint and the pension credit, are 2 percent below last year.

As

I make the bridge from The Post to Newsweek, I’d like to tell you how

excellent journalistic performance at both has been.

Awards don’t measure it, but The Post’s two Pulitzers were gratifying

indeed,

and Newsweek continues to reap acclaim for

its coverage of September 11 and its aftermath, most recently winning

the National Magazine Award for General Excellence, the industry’s

biggest prize.

Circulation remains exceptionally strong, and in many respects the envy of the newsweekly field. In 2001, the magazine broke all existing records for newsstand sales – turning in weekly sales that averaged 80 percent higher than the year before. While there is no chance we’ll repeat that performance, the surge in subscription sales provided by Newsweek’s 9/11 coverage and the war on terror has led to lasting benefits.

Thanks to new business and strong renewals,

Newsweek is providing a bonus of nearly 200,000 copies to advertisers

over its 3.1 million rate base – all without the use of exotic

electronic premiums favored by our competitors.

Time is now offering something that looks like a Palm Pilot

knockoff to attract new subscribers.

On the advertising front, Newsweek continues

to perform better than most other magazines measured by PIB.

But the numbers are anything but robust.

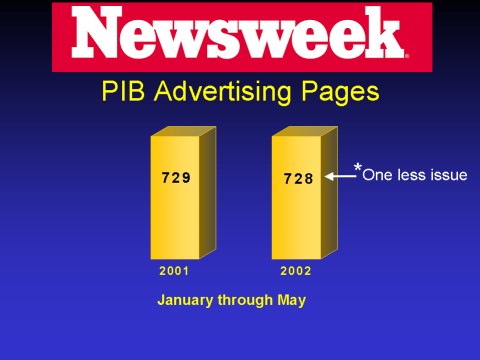

Through the first five months of the year, the magazine is

running virtually even with last year’s pace, although we’ve had one

less issue this year. We

see some indicators of a recovery in the second half, but it is far too

early to take that to the bank. As

always, the fourth quarter remains critical to Newsweek’s performance

for the year.

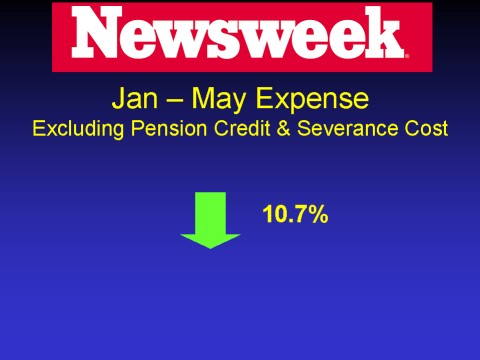

Excluding pension credit and severance

costs, Newsweek’s expenses were down 10.7 percent through May.

I’ve been talking about building value at Cable ONE and Kaplan. In closing, I want to report two things to you.

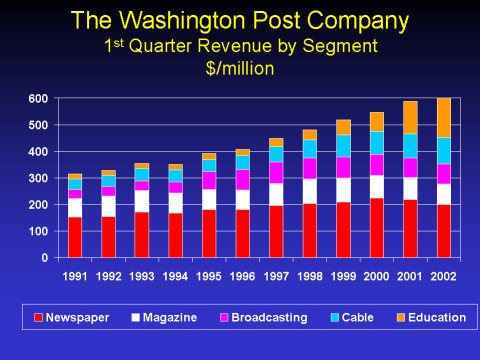

First, here is the revenue growth of the

company by segment. Education

and cable are the top 2 bars: education is gold; cable is blue.

As you know, we don’t provide forecasts. But I wanted to give you a sense of the impact of Kaplan’s

and cable’s substantial revenue growth on the company. So, these are first quarter results for the past 12 years

through the first quarter of 2002.

You can evaluate the growth for yourselves.

Despite the fall-off in our advertising-based units, revenue is

up even in the past two years. We

have built two businesses in Kaplan and Cable ONE that are not

advertising dependent. Their

growth alone will produce good results for the company this year and

beyond.

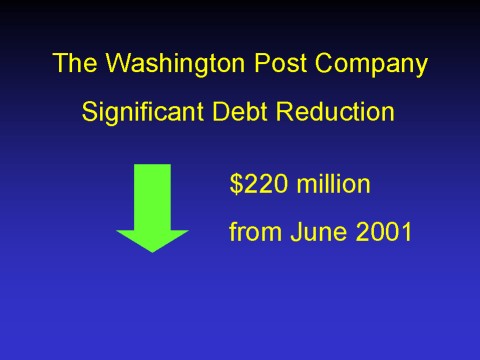

Second, this revenue growth has translated

into substantial improvement in cash flow and the company’s debt

position. Debt reduction

remains a primary focus for the company.

Today, our debt is approximately $820 million, down $220 million

from when I spoke to you last year. This despite continued acquisition

activity and heavy capital spending in the second half of 2001.

Thanks for your attention. Now Jay and I will be happy to answer your questions.

# # #