![]()

Note 7: Pension Plans

|

The company has noncontributory

pension plans which provide defined benefits to domestic and

non-U.S. employees meeting age and length of service

requirements. The following disclosures include amounts for

both the U.S. and significant foreign pension plans. Pension

cost determined in accordance with plan provisions is

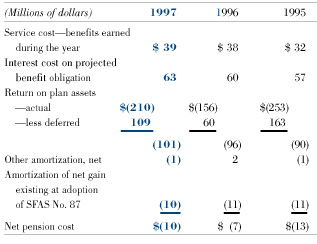

presented below:  Pension cost includes the following

components:  The early retirement and severance benefit programs resulted in a pre-tax gain of $4 million, $2 million and $1 million in 1997, 1996 and 1995, respectively, as settlement gains from retirees electing lump-sum distributions exceeded the cost of the special termination benefits. |

|

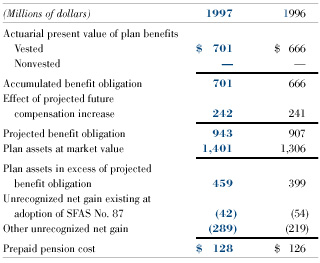

The funded status of these plans at

year end was as follows:  Net assets of the pension trusts, which primarily consist of common stocks and debt securities, were measured at market value. For U.S. plans, the assumed long-term rate of return on trust assets was 8.5% in 1997 and 1996. Pension benefit obligations were determined from actuarial valuations using an assumed discount rate of 7% at December 31, 1997, and 1996, and an assumed long-term rate of compensation increase of 5% in 1997 and 1996. Non-U.S. plans assumed an average rate of return on trust assets of 9.0% in 1997 and 1996, an average discount rate for pension benefit obligations of 8.0% in 1997 and 8.3% in 1996, and an average long-term rate of compensation increase of 6.2% in 1997 and 6.1% in 1996. The company transferred excess pension plan assets of $13 million in 1997 and $13 million in 1996 to fund retiree medical expenses as allowed by U.S. tax regulations. The company has a noncontributory, unfunded pension plan which provides supplemental defined benefits to U.S. employees whose benefits under the qualified pension plan are limited by the Employee Retirement Security Act of 1974 and the Internal Revenue Code. These employees must meet age and length of service requirements. Pension cost determined in accordance with plan provisions was $6 million in 1997, $7 million in 1996 and $6 million in 1995. Pension benefit payments for this plan were $4 million in 1997, $5 million in 1996 and $3 million in 1995.

|

|

|

||

|

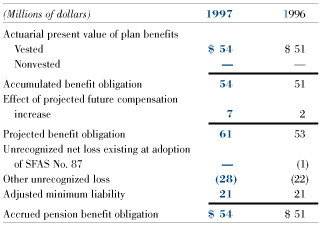

In 1995, the company established a nonqualified trust, referred to as a "rabbi" trust, to fund benefit payments under this pension plan. Trust assets are subject to creditor claims under certain conditions and are not the property of employees. Therefore, they are accounted for as corporate assets and are classified as other non-current assets. Assets held in trust at December 31, 1997 and 1996 totaled $25 million and $21 million, respectively. The status of this plan at year end was as follows:  Pension benefit obligations were determined from actuarial valuations using an assumed discount rate of 7% at December 31, 1997, and 1996, and an assumed long-term rate of compensation increase of 5% in 1997 and 1996. In 1997 the company instituted a nonqualified savings plan for eligible employees in the United States. The purpose of the plan is to provide additional retirement savings benefits beyond the otherwise determined savings benefits provided by the Rohm and Haas Company Employee Stock Ownership and Savings Plan (the "Savings Plan"). Each participant's contributions will be notionally invested in the same investment funds as the participant has elected for investment in his or her Savings Plan account. For most participants, the Company will contribute a notional amount equal to 60% of the first 6% of the amount contributed by the participant. The Company's matching contributions will be allocated to deferred stock units. At the time of distribution, each deferred stock unit will be distributed as one share of Rohm and Haas Company common stock. Contributions to this plan were immaterial in 1997.

|

|

|

Return to Financial Table of Contents