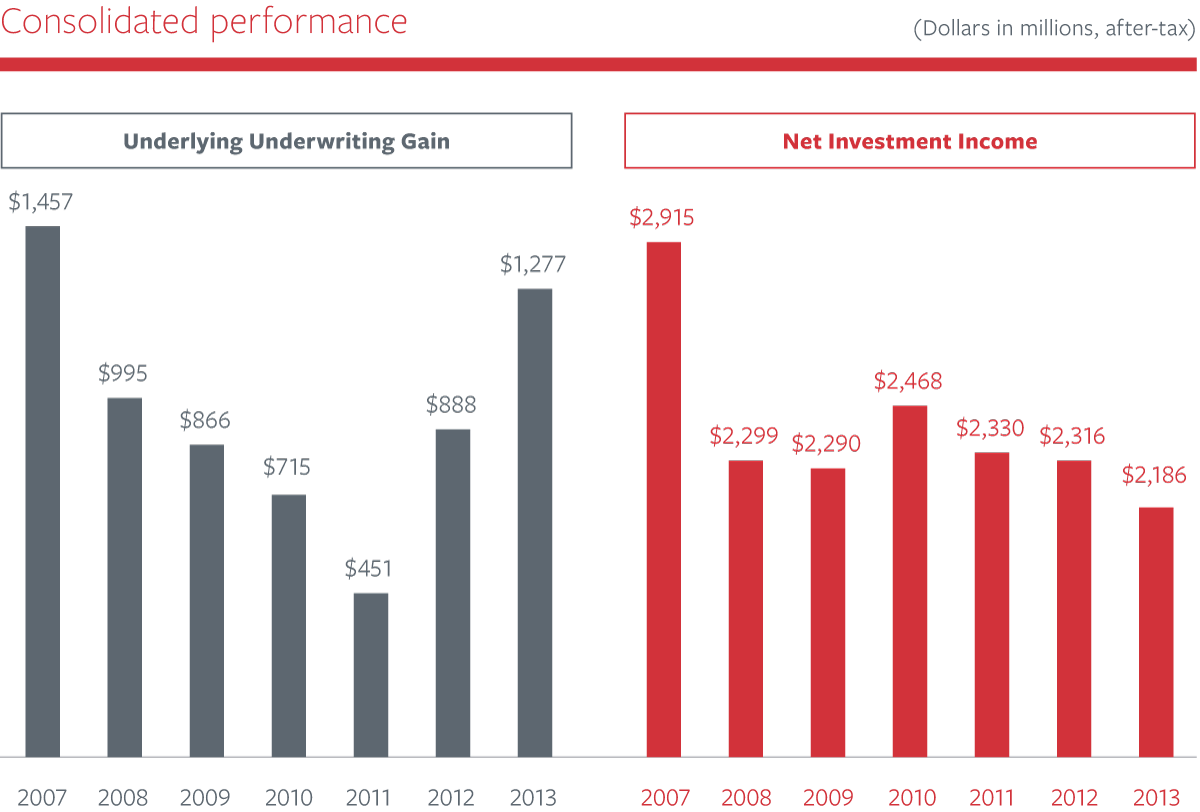

Travelers had a terrific 2013 despite what remains a challenging business environment. We posted net income of approximately $3.7 billion, reflecting strong underlying underwriting margins across our business segments, continued contributions from favorable prior year reserve development, more modest catastrophe losses than in recent years and solid net investment income.

We delivered record net income per diluted share of $9.74, up 55 percent from 2012, return on equity of 14.6 percent and an operating return on equity of 15.5 percent. We ended the year with a book value per share of $70.15, an increase of 4 percent over the prior year-end, and we returned more than $3 billion to our shareholders through share repurchases and dividends.

Each of our business segments contributed to the company's profitability. Our Business Insurance GAAP combined ratio in 2013 improved 5.5 points to 91.9 percent from 2012, and we posted record high net written premiums of $12.2 billion, up 3 percent from 2012. Our Financial, Professional & International Insurance GAAP combined ratio of 84.3 percent in 2013 was essentially unchanged from 2012, and our Personal Insurance GAAP combined ratio in 2013 improved 13.0 points from 2012 to 88.9 percent.

We could not be more pleased with our performance in 2013 and the value we created for our shareholders. It is a testament to our great strength as underwriters on both sides of the balance sheet.

It has been ten years since the insurance company you know today was formed by the merger of Travelers Property Casualty Corp. and The St. Paul Companies, Inc. Over the last decade, we have supported our customers and agents during a period in which the United States experienced some of the costliest natural catastrophes on record, as well as a deep recession precipitated by the global financial crisis.

In order to achieve our return objective, we will continue to execute on this strategy to seek improved returns on our products — particularly as we expect volatile weather to persist and interest rates to remain low.

We are proud of our results in 2013, but we also understand that past achievements are no guarantee of future performance. We remain committed to underwriting fundamentals as we adapt to changes in the broader economic and business environment and address emerging risks in new and innovative ways.

As a general matter, we insure the output of the economy. Consequently, our ability to grow our business is challenged in a low-growth economic environment. We are not going to respond by changing our approach to balancing risk and reward — either in our underwriting or in our investment activities. Instead, we will continue to develop better products for our agents and customers, enhance services and capabilities, and invest in technology to increase efficiency and improve our customers' experience. We will continue to be creative and inventive, bringing our data and analytics expertise and our significant resources to bear to help our agents and customers manage risk.

We also will continue to look at attractive opportunities outside the United States. Our acquisition of Dominion last year was one such opportunity, and one that has given us an exceptional platform from which to expand our commercial lines business in Canada.

We remain committed to underwriting fundamentals as we adapt to changes in the broader economic and business environment and address emerging risks in new and innovative ways.

In the evolving and dynamic insurance industry, change can be rapid and dramatic — as we have seen in the automobile insurance market and in the traditional reinsurance market, where alternative sources of capital have been introduced. Technology also has played an important role by altering the ways products are developed and distributed and by offering new methods for interacting with customers.

To remain competitive in the face of change, we are constantly recalibrating. For example, the adoption of comparative rating technology by independent agents, customers' changing expectations, and our efforts to raise rates had all meaningfully affected our new auto business volume. In response, in 2013 we introduced Quantum Auto 2.0, a more competitively priced product supported by significant expense reduction initiatives, which we developed with input from agents to meet the needs of a broader customer segment increasingly focused on value. We are very encouraged by initial market response.

Remaining true to our core as underwriters who thoughtfully balance risk and reward, we will keep taking actions such as these to remain an industry leader and to continue to deliver shareholder value.

To remain competitive in the face of change, we are constantly recalibrating.

The strong foundation we have built over 160 years is rooted in our commitment to our employees and the communities in which they, our customers and our agents live and work. Over the last five years, Travelers and Travelers Foundation have given more than $100 million to charitable and community organizations. We are pleased that for the seventh consecutive year, we were named to one of the Dow Jones Sustainability Indices in recognition of our business practices and our commitment to delivering meaningful contributions to our communities. We also are proud to have been recognized by both DiversityInc and G.I. Jobs magazines for initiatives that promote inclusion.

I want to express my gratitude to all of the individuals who helped make this a tremendous year for Travelers. I am thankful for the incredible dedication and talent of our employees, the support and partnership of our agents and brokers, and the leadership and guidance of our Board of Directors.

Jay S. Fishman, Chairman and Chief Executive Officer

On Nov. 1, 2013, we completed our acquisition of The Dominion of Canada General Insurance Company, significantly strengthening Travelers' presence in Canada. Travelers and Dominion are a strong strategic fit with complementary businesses.

— Dominion's extensive distribution network and established customer base provide an exceptional platform for expanding the commercial lines business in Canada.

— Combining Travelers Canada's existing surety, management liability and commercial middle market portfolios with Dominion's small commercial and personal products creates an organization with significant product breadth and a balanced mix of businesses.

— The integrated organization will leverage enterprise competitive advantages, including underwriting expertise, sophisticated data and analytics, and leading claim and risk control capabilities.

We focus our giving primarily on education. We also help strengthen communities by fostering small business development, and supporting community developments and the arts to sustain vibrant communities. In addition, our employees contribute many thousands of volunteer hours.

— In 2013, Travelers and the Travelers Foundation gave more than $21 million to charitable and community organizations, for a total of more than $100 million over the last five years.

— Travelers EDGE®, our signature education initiative, reached more than 3,200 underrepresented students during the year and provided 116 students with direct financial support.

— Our Small Business Risk Education program, in partnership with Valley Economic Development Center, Women's Business Development Center and Accion Chicago, provided workshops on risk management for 86 small businesses and helped more than 30 develop safety risk management plans.

— We have joined forces with Habitat for Humanity® and the Insurance Institute for Business and Home Safety to help communities build fortified homes to better withstand future storms in coastal regions of the country.

The Travelers Institute provides thought leadership on critical issues facing our industry.

— The Small Business-Big Opportunity initiative, now in its third year, brought public officials, small business owners and other thought leaders together in Chicago and Boston to elevate the dialogue around small business challenges and opportunities.

— The Institute's third annual “Kicking Off Hurricane Preparedness Season” symposium brought business owners and disaster preparedness professionals to the New York Stock Exchange to discuss lessons learned from Storm Sandy.

— We launched our Consumer Insurance Education Symposia Series in 2013. The program offers insights and information about insurance and personal safety to help people make informed decisions on how to protect their families and assets.

— The Institute screened Overdraft at more than 45 universities. This award-winning nonpartisan documentary, made possible by Travelers in collaboration with public television, highlights the national debt and its implications for individuals and U.S. competitiveness.

The way people buy personal auto insurance has changed dramatically in recent years. Consumers are making purchase decisions based primarily on price — driven largely by price-focused advertising from many auto insurers, consumers' access to pricing information online, and agents' increasing reliance on comparative rating technology for price comparisons.

Travelers launched Quantum Auto 2.0® in 2013. This new auto product offers more competitive pricing to a broader range of consumers. We believe it will help us compete more effectively in the marketplace and will strengthen our relationship with our independent agent partners. In fact, the product was developed in close collaboration with agents.

Quantum Auto 2.0 was available in 18 states at the end of 2013, and we expect to roll it out to the majority of states in 2014.