Basic HTML Version

8

REL I ANCE STEEL & ALUMINUM CO.

GROWING OUR FAMI LY

9

SHAREHOLDER LETTER

acquisition to-date. Metals USA added 44 strategically

located service centers across the United States,

complementing our customer base, product mix, and

geographic footprint. The transaction was immediately

accretive to our bottom-line results and provided us the

opportunity to identify certain areas where we could

rationalize facilities, reducing our overall costs, and allowing

us to more efficiently service our customers. The level

of support and cooperation exhibited between existing

Reliance companies and the newly acquired Metals

USA operations has been fantastic and we are extremely

pleased with the progress we have made by integrating

Metals USA into the Reliance family of companies.

In November, we acquired Haskins Steel Co., Inc., a

processor and distributor of primarily carbon steel and

aluminum products of various shapes and sizes to a

diverse customer base in the Pacific Northwest. Haskins,

headquartered in Spokane, Washington, will enhance

our penetration into this important geographic region.

Since our IPO in 1994, we have completed a total of 56

acquisitions. Today, we are the largest metals service

center company in North America with significant potential

TO OUR SHAREHOLDERS:

In spite of difficult market

conditions that persisted throughout the year, our

strong performance in 2013 was a testament to our

operational excellence coupled with our ability to

consistently execute on our growth strategies. Overall,

demand in 2013 ended up essentially flat compared

to 2012, though we did see momentum building in

the second half of the year. Reliance’s tons sold on a

same-store basis increased approximately 1% in 2013.

Including the impact of acquisitions, total tons sold

increased significantly resulting in net sales of $9.2

billion in 2013, an increase of 9.3% over the prior year.

Market pricing had a significant impact on our profitability.

Our average selling price per ton sold was down 10%

from the prior year, resulting in lower earnings for the

current year despite the higher levels of net sales.

However, strong performance by our managers in the

field resulted in gross profit margins holding relatively

steady in 2013 versus 2012. This consistent execution

reflects our commitment to remaining highly focused on

managing all aspects of the business that are within

our control, which continues to mitigate much of the

impact of the challenging pricing environment.

Based on MSCI data, Reliance continued to surpass the

broader metals service center industry, due mainly to sales

from our acquisitions as well as a slow but steady recovery

in demand. Reliance’s outperformance of the metals

service center industry is further evidence of our ability to

augment organic growth with strategic acquisitions along

with our excellent track-record of operational and financial

excellence and our commitments to safety, employee

satisfaction, and customer service.

Our success in 2013 was also due in part to our

exposure to higher-growth industries, such as commercial

aerospace, energy and automotive. The specialty

products and processes required in these industries

command higher average selling prices and helped

improve our overall profitability. Of note, our automotive

end-market, which we support mostly through our toll

processing operations in the U.S. and Mexico, was one

area of our business that exhibited particular strength

in 2013.

One of the most important highlights of 2013 was the

completion of the Metals USA Holdings Corp. acquisition

in April for a purchase price of $1.25 billion, our largest

for continued growth in a highly fragmented industry.

Our acquisition strategy supports our ability to profitably

grow Reliance, even when faced with economic and cyclical

headwinds. Going forward, acquisitions will remain an

important element of our overall growth strategy. We expect

to continue to be a consolidator in our highly fragmented

industry by making strategic acquisitions of well-managed

metals service centers and processors with end-market

exposure that supports our diversification strategy.

Our balance sheet remains strong, providing us ample

flexibility to leverage potential future growth opportunities

through both internal investments and acquisitions.

After funding our acquisition of Metals USA, including

the issuance of $500 million of 4.5% ten-year senior

notes, we used excess cash to pay down $330 million

of debt in 2013. We will continue to take a balanced

approach to debt reduction while still supporting our

working capital needs, investing in capital expenditures,

and paying our quarterly dividend. Our 2013 cash flow

from operations was over $633 million due to solid

working capital management, which helped to fund our

capital expenditures of $168 million, the majority of

which was spent on growth activities.

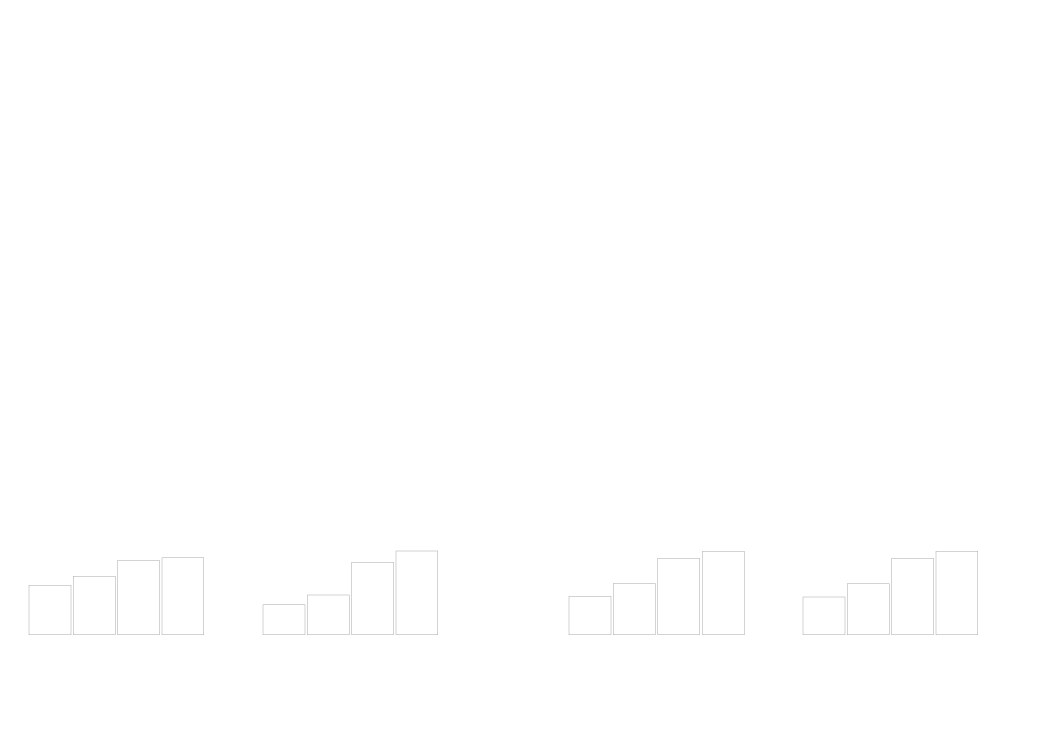

NET SALES (IN MILLIONS)

EARNINGS PER SHARE (DILUTED)

NET INCOME (IN MILLIONS)

RETURN ON EQUITY

2013

2013

2013

2013

2012

2012

2012

2012

2011

2011

2011

2011

2010

2010

2010

2010

2009

2009

2009

2009

$9,223.8

$4.14

$321.6

9%

$8,442.3

$5.33

$403.5

13%

$8,134.7

$4.58

$343.8

12%

$6,312.8

$2.61

$194.4

8%

$5,318.1

$2.01

$148.2

6%