Cincinnati Financial Corporation

The Cincinnati Insurance Companies

The Cincinnati Insurance Companies

|

|

Cincinnati Financial Corporation The Cincinnati Insurance Companies |

March 26, 2008

To Our Shareholders, Friends and Associates:

Your company achieved record operating income in 2007, even as the commercial property casualty insurance market experienced its fourth consecutive year of pricing declines. For the first time in our history, property casualty written premiums for the full year declined. We expected heightened competition and lower premium revenues to erode insurance underwriting profitability; instead, we saw offsetting benefits that led to a record $306 million in underwriting income.

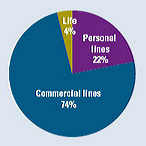

Early in 2008, we already see weather that is not as gentle; an economy and financial markets that are less certain; and daily reminders that intense price competition remains. Once again, we are bracing ourselves for lower premium pricing and the higher loss and expense ratios such pricing causes. If current trends continue, our 2008 premiums could fall as much as 5 percent and our combined ratio could rise to the 96 to 98 percent range, compared with the 1.9 percent premium decline and healthy 90 percent ratio in 2007. We know we have to work harder and win more accounts just to slow the decline or stay even. To move ahead we have to seize new opportunities. In any environment, our agent-centered, relationship-based approach to doing business brings opportunities to grow and prosper. We believe that our local independent agents have the confidence of policyholders in their communities. Both our agents and our policyholders choose Cincinnati policies because they are seeking quality insurance experiences that reward that confidence. To honor our relationships, create loyalty and increase growth over the long term, we must have the courage and persistence to respond to challenges in a distinctly Cincinnati way. We intend to optimize your company's advantages by preserving and extending a unique Cincinnati experience to our agents and policyholders. Commercial Lines:

The Cincinnati Experience – Selling Value and Service With the continuing soft market for commercial insurance, carriers that want to grow are competing very aggressively and sometimes taking underwriting shortcuts. In this environment, we will price flexibly to protect our proven, high-quality renewal accounts. When we quote new business for our agents, we similarly insist that pricing must correlate with the quality of the risk. Because our quote often isn't the lowest, this selectivity compels us to offer special value and service advantages that our agents can sell. Top Claims Service

That value begins with good claims service. Business Insurance reported in December on a recent survey of 13,000 commercial insurance buyers whose firms had revenues ranging from $10 million to $500 million. A larger percentage of respondents considered their satisfaction "excellent" for Cincinnati than for any other carrier. The survey evaluated willingness to pay claims, claims coordination with the agent and claims responsiveness. In 2008, we are increasing claims service satisfaction by giving our agents online access to claims information. Updated Products and Markets

We're updating coverage products in 2008 to make our policies more attractive, including a new optional endorsement that protects against liability arising from a business's use of Web-based technology. Our contractor policyholders will benefit from our new, streamlined process to issue surety bonds for single projects up to $250,000 or total projects up to $400,000. Our local agents are well positioned in their communities to write contractor accounts, which represent a significant portion of our general liability book of business. We will continue in 2008 to serve our agents' construction accounts, while seeking to complement this business by writing more property-dominant accounts. Availability of Excess and Surplus Policies

At the beginning of 2008, we launched two new subsidiaries for the purpose of becoming a market for our agents' excess and surplus lines accounts. Now we are offering more flexible, limited coverage for commercial accounts with special risk characteristics that cannot obtain coverage using state-regulated policy forms and rates. The Cincinnati Specialty Underwriters Insurance Company qualified for an A.M. Best Co. rating of A (Excellent) and began writing general liability E&S policies in five states in January. Over 2008, we plan to add property, miscellaneous professional and excess casualty. Through CSU Producer Resources, our new insurance brokerage that exclusively serves appointed agents of The Cincinnati Insurance Company, we plan to offer E&S policies by year-end 2008 in all 34 states where we market commercial lines. Opportunities to write E&S policies may help us offset the continued decline in our commercial premiums. Agents welcome our entry because we are bringing the Cincinnati experience – our relationship-based approach – to this market. Our E&S underwriters responsible for policy pricing and issuance seamlessly perform the additional functions of E&S brokers. Our E&S philosophy is integrated with our standard lines philosophy: We value and trust the agent's local knowledge. Agents perform frontline underwriting, with access to our commercial lines field marketing representatives. Agents and their clients get full support including underwriting, claims and loss control services, effective processing technology and compensation comparable to our standard market commissions. Improved Agent-facing Technology

Technology improvements are helping our agents meet client preferences and respond efficiently to policyholder inquiries. Agencies in the 19 states where we use our e-CLAS® system to process businessowners policies recently began using our new direct bill payment option, CinciBill™. By year-end, we expect to offer e-CLAS with CinciBill in 31 of our 34 active states and to make substantial progress toward a direct bill solution for policies not processed through e-CLAS. Additionally, we plan to introduce online policy viewing, already available to our associates for more than 75 percent of commercial policies, to our agents in 2008. Multi-year Policy Periods

While all of these new initiatives will help us compete on value and service, one of the most effective sales advantages we give agents has been around for a long time. Ninety percent of our commercial packages have multi-year terms, providing stability to agents and policyholders.

We commit to maintaining over the entire period our same policy provisions and rates on selected coverages, including property, general liability, inland marine and crime. Other coverages in the package are written and priced annually. In return for this security, the policyholder has no downside, remaining free to continue the policy or not. In fact, few opt out. The company and our agents benefit from lower annual administrative expenses, as well as persistency that rises to a very high 96 percent at the interim annual anniversaries of multi-year policies. Personal Lines:

The Cincinnati Experience – Building Scale In personal lines, we work to support the strengths of our local independent agents, who benefit from opportunities to prove their value to people who are centers of influence in their communities. Individuals relying on our home and auto policies receive the same claims service with a human touch that our commercial policyholders enjoy, including prompt, personal responses rather than service-center responses. To effectively support our agents in personal lines, going forward, we need to reduce our expenses, manage geographical risk concentrations and price more accurately. Our agents generated a 16.9 percent increase in new personal lines business in 2007, and we believe the changes we are making have us heading in the right direction. To make further progress and leverage our product and service advantages into the future, we believe we must add to our scale in 2008. 2008 plans include new agency appointments and geographical expansion for personal lines. Currently, all six of our personal lines of business are available in only 22 states, compared with 34 for commercial lines. Opening for business in some of those untapped states would help spread and reduce our catastrophe risk. With scale, we can continue our investment in updated automation, spreading the expense across a larger premium volume to improve our profitability. Finally, we can implement more pricing points based on risk data, fine-tuning our rates for each risk to produce very competitive premiums for our agents' higher quality accounts. Only by receiving these benefits of scale can we assure our agents' access to a competitive, stable personal lines market. Ample Room to Grow

We see many opportunities to jump start personal lines expansion in 2008. Agents in 17 states accounting for 97.5 percent of our premium volume were using our Web-based personal lines policy processing system at year-end. Now we are picking up the pace to roll out to eight more states in 2008. In two of those states – Maryland and North Carolina – our automation makes it practical to market some lines of business for the first time. In three others – Arizona, South Carolina and Utah – our agencies have been waiting for Cincinnati personal lines while writing only commercial business. They represent other personal lines carriers, but many are interested in gaining the advantages of Cincinnati claims service and products for their personal lines clients. This expansion enlarges our footprint outside of the Midwest and Southeast, increasing geographic diversification. Data Plus Knowledge = Selection

We continue to position for growth by steadily improving our policy credits and rates. When our policyholder insures both a home and auto, in many states we now can apply a premium credit to the homeowner policy, as well as continue to credit the auto policy. Another 2008 initiative will increase our inclusion in popular online tools agents and policyholders use to compare carriers. We plan this year to further segment our rates, adding multiple pricing points based on risk-specific data, while also retaining the Cincinnati territory rating approach that recognizes local and regional differences. Though our pricing will reflect quantifiable characteristics, risk selection and underwriting will continue to rely on the agent's knowledge and evaluation of each risk. Proven Policies

Our efforts to grow also hinge on product superiority. Our philosophy has been to include coverages or terms and conditions that give the policyholder some advantage beyond the typical policy. While many carriers have reduced or eliminated earthquake coverage, we continue in most geographical areas to build it into our executive homeowner policies, recognizing that over the past century earthquakes have caused insured property damage in every state. Our Executive Classic™ has many such points of difference, from coverage for earthquakes and landslides to hydrostatic water pressure, as well as ordinance or law coverage up to the dwelling limit. In 2008, an optional endorsement to our homeowner policies will add mechanical breakdown coverage for major home systems such as heating and air conditioning, which are not covered in typical homeowner policies. Life Insurance:

The Cincinnati Experience – Distribution and Product Simplicity The Cincinnati Life Insurance Company operates within an industry characterized by complex distribution systems and ultra sophisticated, changing products. As a life insurer within a property casualty focused organization, we determined that the best way to bring value to our agents, our policyholders and our company was to commit to the independent agency system and to maintain a simple, up-to-date product portfolio. Following this strategy, we have raised policy face amounts in force at a rate of 16.8 percent annually, to $62 billion in 2007 from $18 billion at the beginning of 1999.

Term and Worksite, a Natural Fit

We are preparing to introduce features in 2008 that will make us more competitive by increasing our rating flexibility. Banded rates will apply different factors to policies with higher face amounts. A new Super Select Plus rate classification will allow us to further refine rates based on the health of the applicant. All of our term insurance products and all products available to employees through our worksite marketing program will be updated to assure they are competitive. The simplicity of our term insurance products, along with our distinctive return-of-premium option, appeals to our agents. The worksite program is a natural fit that can help Cincinnati's policyholders with small commercial businesses offer voluntary benefits to staff through payroll deduction. Plans for this year include extra support for agents who cross-sell life policies to the company's personal lines policyholders. Investment:

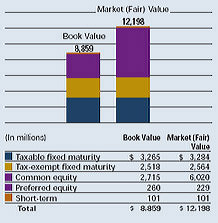

The Cincinnati Experience – Selecting and Managing for Quality Uncertainty and instability have prevailed in the financial markets over recent months. One source of uncertainty has been the property casualty industry's potential exposure to the credit markets, including sub-prime mortgages. Our investment portfolio contains no mortgage loans. Our bond portfolio, which has no mortgage-backed securities, continues to hold steady. The flight to quality and the resulting lower rates for risk-free securities supported bond valuations, helping to offset the effects of increasing risk premiums and credit spreads in the last quarter of 2007. We believe that the market may have judged our company's portfolio too harshly on this score in the short term and that we are well positioned for the long term. We have a substantial municipal bond portfolio, selected for yield and quality, consisting of securities backed by general obligations and essential services revenues. Municipal bonds representing about 87 percent of that portfolio's value are insured. Although many of the bond insurers are suffering some well publicized problems, our average underlying ratings are strong for our insured bonds, minimizing our potential downside risk.

Turning to our equity portfolio, banks and other financial sector stocks make up about 55 percent of our equity portfolio and about 35 percent of your company's total investment portfolio. This concentration offers us the advantages of good dividend income but exposes us to market volatility when sector issues arise. Needless to say, the sector is under pressure. To varying degrees, the financial services firms in our portfolio are addressing a challenging credit quality environment and related issues. Some of our holdings are evaluating their dividend levels in light of their own capital requirements and earnings outlook, potentially slowing our investment income growth. We emphasize portfolio strategies to maximize both income and capital appreciation over the long-term and we are monitoring our holdings in the financial sector closely. We remain committed to sustaining strong capitalization. Consistent and Transparent

We adhere to our investment philosophy, working to assure the credit quality of our bonds and to selectively invest in blue chip, dividend-paying stocks per our stated criteria: we look for common stocks with increasing sales and earnings, proven management, favorable outlooks, annual dividend yields that meet or exceed that of the overall market and have the potential for future dividend increases as well as price appreciation. Our cash flow from healthy insurance operations has always been adequate to fund our insurance liabilities. This success on the insurance side of our operations supports the investment side, giving us the flexibility to follow our total return, buy-and-hold approach. You can see exactly what securities your company owns at any time by reviewing our quarter-ending portfolios on the Investor's page of www.cinfin.com. Year After Year

Your company's board of directors is committed to producing steady value for shareholders. We returned $546 million to shareholders during 2007, including $306 million through repurchases of our common stock and $240 million of cash dividends paid. Record repurchase activity in 2007 included an accelerated stock repurchase under which we bought 4 million shares. In authorizing the ASR, the board also increased its repurchase authorization to an additional 13 million shares. In February 2008, the board of directors authorized a 9.9 percent increase in the regular quarterly cash dividend to an indicated annual rate of $1.56 per share. This action set the stage for a 48th consecutive year of increase in that measure. That track record shows that we are working for a positive year-after-year experience for you, our shareholders, as well as our agents, policyholders and associates. In this era when year-over-year success is the goal usually measured, we promise to look further down the road, choosing actions that help Cincinnati stand out from the competition and rewarding your confidence. Respectfully,

This report contains forward-looking statements that involve potential risks and uncertainties. For factors that

could cause results to differ materially from those discussed, please see the most recent edition of our safe

harbor statement under the Private Securities Litigation Reform Act of 1995. To view or print the edition in

effect as of this report's initial publication date, please view this document as a printable PDF.

|

|||||||||||||||||||||||||||||||||||||||||

|

Shareholder Information |

Financials & Analysis |

Business Information |

Ratings |

Electronic Delivery |

Investor Contacts |

Safe Harbor | Individuals & Families | Businesses & Organizations | Investors | Independent Agents | Career Seekers | Identity Protection, Phishing and Fraud Home Terms and Conditions Privacy Policies Copyright © 2008, Cincinnati Financial Corporation Investor Contacts |

|||||||||||||||||||||||||||||||||||||||||

View this document as a printable PDF (.5 MB)

View this document as a printable PDF (.5 MB) Get Adobe Acrobat Reader

Get Adobe Acrobat Reader View all printable Documents

View all printable Documents

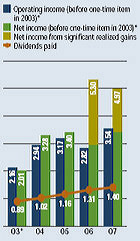

In 2007, realized investment gains of

$382 million reflected four significant

transactions greater than $50 million –

the sale of shares of Exxon Mobil

Corporation, the block sale of shares

of Fifth Third Bancorp, the sale of our

holding in FirstMerit Corporation and the

disposition of the majority of our holdings

in real estate investment trusts. In 2006,

realized investment gains of $684 million

largely were from the sale of our holding

in Alltel Corporation.

In 2007, realized investment gains of

$382 million reflected four significant

transactions greater than $50 million –

the sale of shares of Exxon Mobil

Corporation, the block sale of shares

of Fifth Third Bancorp, the sale of our

holding in FirstMerit Corporation and the

disposition of the majority of our holdings

in real estate investment trusts. In 2006,

realized investment gains of $684 million

largely were from the sale of our holding

in Alltel Corporation.