Dear Fellow Shareholders,

In 2009, Walter Investment Management Corp. demonstrated that it is one of the top asset managers and specialty mortgage servicers in the nation, achieving strong performance from our less-than-prime portfolio in the face of the most challenging economic environment in decades. This solid performance allowed us to produce 2009 income before income taxes and spin-off related costs of $39.7 million, and pay quarterly dividends of $0.50 per share.

Our accomplishments are attributable, quite simply, to the great people we have in our company. Our employees produced superior results, while also preparing for and executing the transactions that created our stand-alone public company and establishing the solid foundation for our future growth and success.

Our field servicing organization's commitment, combined with our tested and proven high-touch servicing approach, produced superior results from our less-than-prime portfolio during the worst economic environment of our company's history.

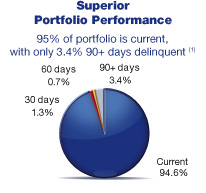

- Consolidated delinquencies were 5.44 percent at year's end, and when calculated on a comparable basis are better than the most recently released Mortgage Bankers Association's subprime industry survey average by more than half.

- Average delinquencies for the year were up only 15 percent from the average for the previous five-year period, despite a rise in unemployment rates to over 10 percent.

- Recovery rates averaged 84 percent for the year, down only slightly from the previous five-year average of 86 percent, despite significant and widespread home price depreciation across the country.

Our corporate employees provided much-needed support to the field servicing organization without interruption, while also transitioning us to a stand-alone public company with all the functions and systems needed by that company.

- The new company was formed on April 17, 2009 after the spin-off of our business from Walter Energy, Inc. and a merger with Hanover Capital Mortgage Holdings, Inc.

- Our management team accomplished much in a short timeframe, establishing the new functions required to support a public entity. Further, over the course of the year, management has made a concerted effort to communicate the key aspects of our operations and strategy to shareholders and potential investors.

- We raised $76.8 million from the sale of common equity, giving us the financial resources needed to seize opportunities for growth.

At WIMC, we indeed have an engaging story to tell. Our methods of operation — anchored in more than 50 years of solid experience underwriting mortgages, coupled with a high-touch, personal approach to servicing our customer relationships — have allowed us to weather a tremendous storm in the mortgage industry.

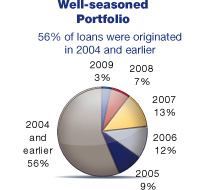

Our performance today is aided by the fact that we maintained our underwriting discipline and didn't open the floodgates for approvals in recent years as many competitors did. With over half our loans originated in 2004 and earlier, we have a portfolio of well-seasoned loans, with less exposure to the bubble in real estate values that has created so many issues over the past two years.

How we service our assets is also critical. Our approach is designed to try to keep customers in their homes and making payments when possible — a foreclosure doesn't help anyone. Instead of servicing solely by phone from call centers, our local servicing representatives in the field maintain a high level of contact with customers, visiting with them in person when needed. Our field servicing personnel develop a deep knowledge of their markets and their customers, and have a strong sense of ownership and accountability for the mortgages assigned to them. With this approach, we are able to tackle problems before they get out of hand.

Again, a key to the success of this aspect of our unique business model is our people. Our field servicing organization is led by seasoned managers who have an average of 25 years of experience in the industry. Our local field servicing representatives have an average of six years of experience, and our retention rate among this group is roughly 70 percent annually.

Still, even though we have a long history and track record and use words such as "experienced" and "proven" to describe ourselves, we are not stuck in the past. We continue to make investments in and improvements to our technology and operating systems to build for the future. We are supporting our skilled and experienced field organization with a servicing platform and other infrastructure to allow quick access to the critical information needed to produce continuing improvement in results.

Looking Ahead

With a strong platform in place and financial capital to support our plans for growth, we have two primary goals for 2010:

- Continue producing strong financial results and cash flow from our core business, keeping the existing portfolio's performance at industry-leading levels, even though the economy may recover more slowly than we all hope.

- Take advantage of opportunities in the market and aggressively pursue options to grow our business, leveraging our available capacity and our capabilities as they relate to less-than-prime mortgage assets.

Nationally, there is a staggering level of problem residential loans, currently estimated to exceed $1 trillion and continuing to grow. The FDIC has in excess of $36 billion of assets from failed banks yet to be resolved and listed 702 banks with $403 billion of assets as "problem" banks at December 31, 2009. We believe these numbers indicate that there are ample opportunities to deploy our superior servicing capabilities.

We are taking a wide view of our options. We will consider and evaluate opportunities to buy assets through FDIC transactions, as well as sourcing assets for purchase from private sellers. We will apply leverage to these transactions prudently, to provide financial flexibility and to increase potential returns to our shareholders. However, our investment opportunities are not limited to outright purchases of loans. In addition to opportunities to acquire loans at attractive returns, our servicing capabilities should be extremely attractive to owners of distressed mortgage portfolios who need to improve the performance of their assets. In that vein, we will pursue potential opportunities for new originations, as well as co-investment, partnership and servicing arrangements that could involve our servicing for other holders of distressed assets.

Our successful capital raise gives us the financial capability to move quickly when the right opportunities present themselves. We remain focused on those options that leverage our existing capabilities and capacity, are principally within our geographic footprint, and offer attractive returns.

To assist us in these efforts, we recently announced the addition of Denmar Dixon to the management team. Driving business development efforts, Denmar will be working with me, Charles Cauthen and the rest of the management team to find the right opportunities for our growth in the months ahead.

That said, I promise to you, my fellow shareholders, that we won't take our eyes off the ball as we pursue this growth, knowing that the strength of our existing portfolio is the platform that allows us the opportunity to extend our reach.

We are greatly appreciative of the tremendous efforts and support that our employees, advisors, vendors and shareholders provided us throughout the past year. Your management team is hard at work, with our full focus on making our 2010 goals a reality. At Walter Investment Management Corp., we combine a tradition of excellence with a high-powered, entrepreneurial spirit for growth that positions us extremely well for the future.

Mark J. O'Brien

Mark J. O'Brien

Chairman and Chief Executive Officer

March 10, 2010

(1) Accounts in bankruptcy paying in accordance with their plan are considered current. Delinquency status as of December 31, 2009. Expressed as a percentage of principal balance of residential loans outstanding as of December 31, 2009.

(1) Accounts in bankruptcy paying in accordance with their plan are considered current. Delinquency status as of December 31, 2009. Expressed as a percentage of principal balance of residential loans outstanding as of December 31, 2009.