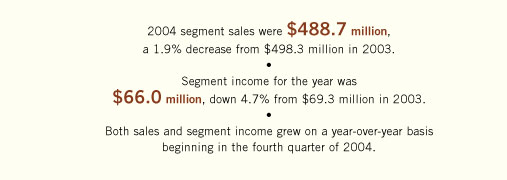

|

While the overall check market continues to decline at an estimated rate of 4% - 5% per annum, Printed Products began to grow again in the fourth quarter of 2004 – registering quarterly increases in both sales and income on a year-over-year basis. This growth, which we expect to continue in 2005, supports our belief that mature markets can still contain growth opportunities.

In the case of Printed Products, these opportunities came from having a value proposition that clearly differentiates us from our competitors and from leveraging investments in technology to improve our operating efficiencies.

Our value proposition focuses on increasing the profitability of financial institutions’ relationships with their customers and increasing the loyalty these consumers have to their bank or credit union. We do not compete with our financial institution customers by marketing directly to the end consumer on our behalf. Instead, we market to end consumers on their behalf. This fact alone sets us apart from our major competitors.

Our integrated expertise in digital technology, business intelligence and applied marketing helps us provide unparalleled support for our customers’ brands. We help these financial institutions in areas that matter to them – such as increasing fee income and net interest margin – as well as in improving efficiency and customer retention.

Our ability to work on behalf of financial institutions extends to both their consumer and small business customers through programs such as HarlandConnect(sm) and HBS Advantage. Through these programs, we use our check-ordering expertise to strengthen relationships and increase the value of each order sold by cross-selling and up-selling related products.

Another example of our value proposition in action is HarlandImpactsm, which combines our Stratics behavioral models and our digital technology. HarlandImpact delivers to individual consumers personalized messages designed to cross-sell and up-sell other products from the financial institution. These targeted messages are inserted in individual checkbooks, rather than as traditional generic fliers in the check box.

This value proposition was originally developed for the community bank and credit union market. Today, financial institutions of all sizes are realizing it can lead to stronger, more profitable relationships with their customers. It was a key factor in Harland Printed Products winning a number of new accounts in 2004, including the largest in the company’s history.

While new product innovation is crucial to growing Printed Products, creating shareholder value requires that we continue to focus on running the business more efficiently as well.

The reorganization of Printed Products that began in 2003 was completed in 2004 – on time and under budget. We reduced our domestic footprint from 14 to 9 production facilities and reduced certain SG&A expenses. We also completed the conversion of our business check and international operations to digital printers and expect to realize the same level of efficiencies here as we did in our imprint facilities.

Harland’s check volumes began increasing in late 2004, and we expect them to increase further on a year-over-year basis in 2005. Average price per unit, however, was down 5.4% in 2004, reflecting a competitive pricing environment and the overall mix of business.

Several years ago, we outsourced customer service for Printed Products, even though it was an area in which we had traditionally excelled. It was the wrong course of action, and we rectified the situation by bringing customer service back in house and investing in training and new systems for our employees. In 2004, our two in-house customer care centers in Atlanta and Salt Lake City were named “Call Centers of Excellence” by Purdue University. This recognition reinforces the tremendous importance we place on customer satisfaction and means both locations perform in the top 10% of all call centers surveyed.

We are also expanding the capabilities of our call centers. They no longer simply take check orders and confirm order status. Today, in addition to handling traditional inbound calls, our customer service representatives increasingly are conducting outbound telemarketing to end consumers on behalf of financial institutions in an effort to increase the value of each order through up-selling and cross-selling other products and services. It is another example of our marketing expertise in action.

Printed Products includes two other businesses: Integrated Client Solutions and Harland Business Solutions.

Integrated Client Solutions includes our Direct Marketing, Investment Services and Analytical Services businesses, which were combined into a single business in 2004. This business decreased almost 5% in 2004, and we do not see a fundamental change in the near future. However, like our core Printed Products business, we see opportunity where others may not. We are especially proud of our analytical services capability, which enables us to identify the next product or service a consumer is most likely to purchase from their financial institution or which customers are most likely to leave their financial institution. Combining this analytical capability with our digital technology and marketing expertise can be a powerful asset for a financial institution.

Harland Business Solutions focuses on computer checks and forms and is another way we serve the small business market. Harland Business Solutions also serves specialty retailers and alternative channels. This business grew 2.5% in the year thanks to both increased volume from existing accounts and a number of new customers.

In summary, we believe we have turned around Printed Products, and we expect it to grow in 2005. Our strategy is to first achieve operating excellence in the check program, which we are able to do because of our digital technology and productivity efficiencies. We then build on that base with sophisticated analytical and marketing products and services. The combination of these capabilities enables us to help financial institutions engage, grow and retain profitable relationships with their customers. |