McCORMICK & COMPANY

2008 ANNUAL REPORT

McCORMICK & COMPANY 2008 ANNUAL REPORT |

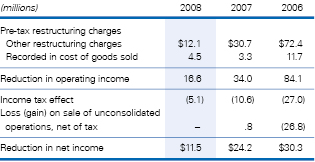

program. The segment breakdown of the total charges is expected to be approximately 65% related to the consumer segment and 35% related to the industrial segment. Of these charges, we expect approximately $100 million will consist of severance and other personnel costs and approximately $50 million for other exit costs. Asset write-offs are expected to be approximately $10 million, exclusive of the $34 million pre-tax gain on the redemption of our Signature Brands, L.L.C. joint venture (Signature) recorded in 2006. We expect the cash related portion of the charges will be approximately $105 million. As of November 30, 2008 the majority of our restructuring program had been completed, although certain parts are still underway and will be completed in 2009.

From inception of the project in November 2005, we have incurred $112.5 million of restructuring charges, including gains on the disposals of our manufacturing facility in 2007 and 2008, the $33.7 million gain recorded on the redemption of our Signature investment in 2006 and other gains from joint ventures in 2006 and 2007. The actions being taken pursuant to the restructuring plan are expected to eliminate 1,325 positions by the conclusion of the plan. Of the expected global workforce reduction, 1,270 positions have been eliminated as of November 30, 2008. |

On the disposition of our Signature investment, the fair value of our investment was $56.0 million as compared to our book value of this unconsolidated subsidiary of $21.7 million. After consideration of transaction costs of $0.6 million and taxes of $7.2 million, we recorded a net after-tax gain of $26.5 million which is shown on the line entitled “(Loss) gain on sale of unconsolidated operations” in our income statement. On the acquisition of the 49% minority interest of DPI, the fair value of these shares was assessed at $46.9 million. Since this business was consolidated, the book value of this 49% share was shown as $29.9 million of minority interest on our balance sheet. After consideration of transaction costs of $0.7 million, we allocated $17.7 million to goodwill. The impact of increasing our share in DPI and disposing of Signature on future net income is not material. |

||