|

|

Notes

to Consolidated Financial Statements

|

|

t

Note 1. Accounting

Policies:

Principles of Consolidation:

The consolidated

financial statements include all significant majority-owned

subsidiaries. Affiliated companies in which Cummins does not

have a controlling interest, or for which control is

expected to be temporary, are accounted for using the equity

method. Use of estimates and assumptions as determined by

management is required in the preparation of consolidated

financial statements in conformity with generally accepted

accounting principles. Actual results could differ from

these estimates and assumptions.

Revenue

Recognition:

The Company recognizes revenues on the sale of its

products, net of estimated costs of returns, allowances and

sales incentives, when the products are shipped to

customers. The Company generally sells its products on open

account under credit terms customary to the region of

distribution. The Company performs ongoing credit

evaluations of its customers and generally does not require

collateral to secure its customers' receivables.

Foreign

Currency:

Assets and liabilities of foreign entities, where the

local currency is the functional currency, have been

translated at year-end exchange rates, and income and

expenses have been translated to US dollars at

average-period rates. Adjustments resulting from translation

have been recorded in shareholders' investment and are

included in net earnings only upon sale or liquidation of

the underlying foreign investment.

For foreign entities where

the US dollar is the functional currency, including those

operating in highly inflationary economies, inventory,

property, plant and equipment balances and related income

statement accounts have been translated using historical

exchange rates. The resulting gains and losses have been

credited or charged to net earnings.

Derivative Instruments:

The Company makes

use of derivative instruments in its foreign exchange,

commodity price and interest rate hedging programs.

Derivatives currently in use are commodity and interest rate

swaps, as well as foreign currency forward contracts. These

contracts are used strictly for hedging, and not for

speculative purposes. Refer to Note 8 for more information

on derivative financial instruments.

The Company enters into

commodity swaps to offset the Company's exposure to price

volatility for certain raw materials used in the

manufacturing process. As the Company has the discretion to

settle these transactions either in cash or by taking

physical delivery, these contracts are not considered

financial instruments for accounting purposes. These

commodity swaps are accounted for as hedges.

Other Costs:

Estimated costs of

commitments for product coverage programs are charged to

earnings at the time the Company sells its

products.

Research & development

expenditures, net of contract reimbursements, are expensed

when incurred and were $228 million in 1998, $250 million in

1997 and $235 million in 1996.

Maintenance and repair costs

are charged to earnings as incurred.

Cash Equivalents:

Cash equivalents

include all highly liquid investments with an original

maturity of three months or less at time of

purchase.

Inventories:

Inventories are

generally stated at cost or net realizable value.

Approximately 25 percent of domestic inventories (primarily

heavy-duty and high-horsepower engines and engine parts) are

valued using the last-in, first-out (LIFO) cost method.

Inventories at December 31 were as follows:

Top

of page

Property, Plant and Equipment:

Property, plant and

equipment are stated at cost. A modified units-of-production

method, which is based upon units produced subject to a

minimum level, is used to depreciate substantially all

engine production equipment. The straight-line depreciation

method is used for all other equipment. The estimated

depreciable lives range from 20 to 40 years for buildings

and 3 to 20 years for machinery, equipment and

fixtures.

Software:

Internal and

external software costs (excluding research, reengineering

and training) are capitalized and amortized generally over 5

years. Effective January 1, 1998, the Company adopted SOP

98-1 on accounting for internal use software costs. Internal

software costs capitalized in 1998 in accordance with this

new rule were $9 million. Capitalized software, net of

amortization, was $75 million at December 31, 1998 and $32

million at December 31, 1997.

Earnings Per Share:

Effective January 1,

1997, the Company adopted SFAS No. 128, a new accounting

rule on calculating earnings per share. Under the new rule,

basic earnings per share of common stock are computed by

dividing net earnings by the weighted-average number of

shares outstanding for the period. Diluted earnings per

share are computed by dividing net earnings by the

weighted-average number of shares, assuming the exercise of

stock options when the effect of their exercise is dilutive.

Shares of stock held by the employee benefits trust are not

included in outstanding shares for EPS until distributed

from the trust. Years prior to 1997 have been restated to

reflect this new rule.

Top

of page

Note 2.

Acquisition: In

January 1998, the Company completed the acquisition of the

stock of Nelson Industries, Inc., for $453 million. Nelson,

a filtration and exhaust systems manufacturer, was

consolidated from the date of its acquisition. On a pro

forma basis, if the Company had acquired Nelson on January

1, 1997, consolidated net sales for 1997 would have been

$5.9 billion and consolidated earnings would not have been

materially different. In accordance with APB Opinion No. 16,

Nelson's net assets were recorded at fair value at the date

of acquisition. The purchase price in excess of net assets

will be amortized over 40 years.

Note 3. Special

Charges: In 1998,

the Company recorded special charges of $92 million for

product coverage costs and inventory write-downs. The

product coverage special charges of $78 million included $43

million primarily attributable to the recent experience of

higher-than-anticipated base warranty costs to repair

certain automotive engines manufactured in previous years,

and $35 million related to a revised estimate of product

coverage cost liability primarily for extended warranty

programs. The Company believed it was necessary to make

these special charges to accrue for such product coverage

costs expected to be incurred in the future on these engines

currently in the field. The special charges also included

$14 million for inventory write-downs associated with the

Company's restructuring and exit activities. These

write-downs relate to amounts of inventory rendered excess

or unusable due to the closing or consolidation of

facilities. The Company has committed to these facility

closures and consolidations as part of a plan to reduce

costs and improve operating performance.

Note 4. Restructuring and Other

Non-Recurring Charges: In

1998, the Company recorded charges of $125 million,

comprised of $100 million for costs to reduce the worldwide

workforce, as well as costs associated with streamlining

certain majority-owned and international joint venture

operations and

$25 million for a civil

penalty to be paid by the Company as a result of an

agreement reached with the U.S. Environmental Protection

Agency (EPA), the Department of Justice (DOJ) and the

California Air Resources Board (CARB) regarding diesel

engine emissions. The major components of these charges are

as follows:

Top

of page

The restructuring program

was undertaken to address the decline in the Company's

business in Asia, to leverage overhead costs for all

operations and to improve joint venture operating

performance.

The charges for

majority-owned operations include $38 million for severance

and related costs associated with workforce reductions of

approximately 1,100 people. These reductions are in the

engine and power generation businesses and are primarily for

administrative positions. Costs for workforce reductions

were based on amounts pursuant to benefit programs and

contractual provisions or statutory requirements at the

affected operations. Approximately one-half of these

employees left the Company prior to December 31,

1998.

The asset impairment loss,

calculated according to the provisions of SFAS 121, was

recorded primarily for engine manufacturing equipment to be

disposed of upon the closure or consolidation of facilities

or the outsource of production. The recovery value for the

equipment to be disposed of was based on estimated

liquidation value. The carrying value of assets held for

disposal and the effect from suspending depreciation on such

assets is immaterial.

Facility consolidation and

other costs of $17 million include lease termination and

facility exit costs of $10 million, product support costs of

$3 million and litigation and other costs of $4 million. As

the restructuring consists primarily of the closing or

consolidation of smaller operations, the Company does not

expect these actions to have a material effect on future

revenues.

The charges for

restructuring joint venture operations totaled $23 million,

the majority of which relates to actions being taken at the

Company's joint venture with Wartsila, which is part of the

Company's power generation business. The charges include $11

million for employee severance and related benefits for

approximately 1,200 people, $7 million for a tax asset

impairment loss and $5 million for other facility and

equipment-related charges.

Approximately $25 million,

primarily related to employee severance, has been charged to

the restructuring liabilities as of December 31, 1998. Of

the total charges associated with restructuring activities,

cash outlays will approximate $60 million. The program is

expected to be essentially complete by the end of 1999 and

yield approximately $50 million in annual savings at

completion.

In addition to the civil

penalty, the agreement with the EPA/DOJ/CARB provides a

schedule for diesel engines to meet certain emission

standards and requires manufacturers to continue to invest

in environmental projects to further reduce oxides of

nitrogen (NOx) emissions. The Company has developed

extensive corporate action plans to comply with all aspects

of the agreement. Additionally, three separate court actions

have been filed as a result of allegations of the diesel

emissions matter. The New York Supreme Court ruled in favor

of the Company. This matter is now on appeal. A California

State Court recently ruled in favor of the Company. A recent

action was just filed in the U.S. District Court, the

District of Columbia.

Note 5. Investments in Joint

Ventures and Alliances: Investments

in joint ventures and alliances at December 31 were as

follows:

Net sales of the joint

ventures and alliances were $1.2 billion in 1998 and $1.3

billion in 1997 and 1996. Summary balance sheet information

for the joint ventures and alliances was as

follows:

The Company has guaranteed

$79 million in outstanding debt of the Cummins Wartsila

joint venture as of December 31, 1998.

In connection with various

joint venture agreements, Cummins is required to purchase

products from the joint ventures in amounts to provide for

the recovery of specified costs of the ventures. Under the

agreement with Consolidated Diesel, Cummins' purchases were

$535 million in 1998 and $538 million in 1997.

Top

of page

Note 6. Long-Term

Debt: Long-term debt

at December 31 was:

Maturities of long-term debt

for the five years subsequent to December 31, 1998 are $26

million, $26 million, $25 million, $27 million and $141

million. At both December 31, 1998 and 1997, the

weighted-average interest rate on loans payable and current

maturities of long-term debt approximated 7

percent.

The Company maintains a $500

million revolving credit agreement, maturing in 2003, under

which there were no outstanding borrowings at December 31,

1998 or 1997. The revolving credit agreement supports the

Company's commercial paper borrowings. In February 1998, the

Company issued $765 million face amount of notes and

debentures under a $1 billion Registration Statement filed

with the Securities and Exchange Commission in 1997. Net

proceeds were used to finance the acquisition of Nelson and

pay down other indebtedness outstanding at December 31,

1997. The Company also has other domestic and international

credit lines with approximately $193 million available at

December 31, 1998.

In 1997, the Company issued

$120 million of 6.75 percent debentures that mature in 2027.

Holders have a one-time option in 2007 to redeem the

debentures and Cummins has a recall right after ten

years.

The Company has guaranteed

the outstanding borrowings of its ESOP Trust. The notes were

refinanced in July 1998. Cash contributions to the Trust,

together with the dividends accumulated on the common stock

held by the Trust, are used to pay interest and principal.

Cash contributions and dividends to the Trust and the

Company's compensation expense approximated $10 million in

each year. The unearned compensation, which is reflected as

a reduction to shareholders' investment, represents the

historical cost of the shares of common stock that have not

yet been allocated by the Trust to participants.

Note 7. Other

Liabilities: Other

liabilities at December 31 included the

following:

Top

of page

Note 8. Financial Instruments and

Risk Management: The

Company is exposed to financial risk resulting from

volatility in foreign exchange rates and interest rates.

This risk is closely monitored and managed through the use

of financial derivative contracts. As clearly stated in the

Company's policies and procedures, financial derivatives are

used expressly for hedging purposes, and under no

circumstances are they used for speculating or trading.

Transactions are entered into only with banking institutions

with strong credit ratings, and thus the credit risk

associated with these contracts is considered immaterial.

Hedging program results and status are reported to senior

management on a periodic basis.

Foreign Exchange

Rates

Due to its international

business presence, the Company uses foreign exchange forward

contracts to manage its exposure to exchange rate

volatility. Foreign exchange balance sheet exposures are

aggregated and hedged at the corporate level. Maturities on

these instruments generally fall within the one-month and

six-month range. The objective of the hedging program is to

reduce earnings volatility resulting from the translation of

net foreign exchange balance sheet positions. The total

notional amount of these forward contracts outstanding at

December 31, 1998, and December 31, 1997, were $174 million

and $257 million, respectively.

Interest Rates

The Company manages its

exposure to interest rate fluctuations through the use of

interest rate swaps. Currently the Company has in place one

interest rate swap that effectively converts fixed-rate debt

into floating-rate debt. The objective of this swap is to

lower the cost of borrowed funds. The contract was

established during October 1998 with a notional value of

$225 million. There were no interest rate swap contracts

outstanding at December 31, 1997.

Fair Value of Financial

Instruments

Based on borrowing rates

currently available to the Company for bank loans with

similar terms and average maturities, the fair value of

total debt, including current maturities, at December 31,

1998, approximated $1,214 million. The carrying value at

that date was $1,227 million. At December 31, 1997, the fair

and carrying values of total debt, including current

maturities, were $664 and $654 million, respectively. The

carrying values of all other receivables and liabilities

approximated fair values.

Note 9. Income Taxes:

The provision for

income taxes was as follows:

Top

of page

The Company expects to

realize all of its tax assets, including the use of all

carryforwards, before any expiration.

Significant components of

net deferred tax assets related to the following tax effects

of differences between financial and tax reporting at

December 31:

Top

of page

Earnings before income taxes

and differences between the effective tax rate and US

Federal income tax rate were:

Top

of page

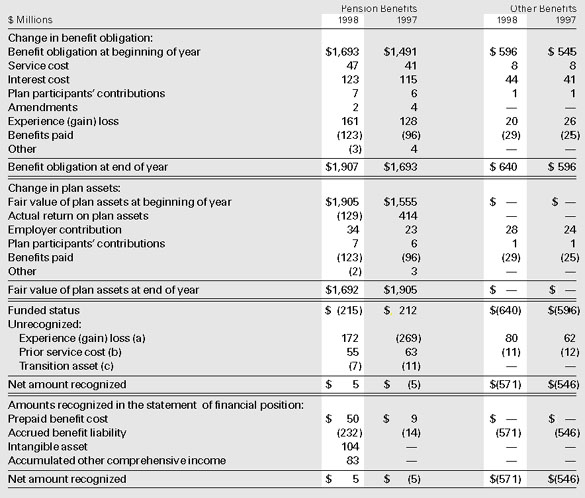

Note 10. Retirement Plans:

The Company has

various contributory and noncontributory pension plans

covering substantially all employees. Cummins common stock

represented 9 percent of pension plan assets at December 31,

1998.

Cummins also provides

various health care and life insurance benefits to eligible

retirees and their dependents but reserves the right to

change benefits covered under these plans. The plans are

contributory with retirees' contributions adjusted annually,

and they contain other cost-sharing features, such as

deductibles, coinsurance and spousal contributions. The

general policy is to fund benefits as claims and premiums

are incurred.

The projected benefit

obligation, accumulated benefit obligation and fair value of

plan assets for plans with accumulated benefit obligations

in excess of plan assets were $1,296 million, $1,251

million, and $999 million, respectively as of December 31,

1998, and $418 million, $381 million, and $339 million,

respectively, as of December 31, 1997. The assumed long-term

rate of compensation increase for salaried plans was 4.25%

in 1998 and 5.0% in 1997. Other significant assumptions for

the Company's principal plans were:

For measurement purposes a

7% annual increase in health care costs was assumed for

1999, decreasing gradually to 4.25% in ten years and

remaining constant thereafter.

Increasing the health care

cost trend rate by one percent would increase the obligation

by $42 million and annual expense by $3 million. Decreasing

the health care cost trend rate by one percent would

decrease the obligation by $38 million and annual expense by

$3 million.

Top

of page

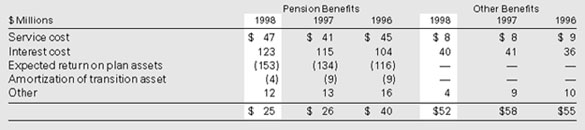

The Company's net periodic

benefit cost under these plans was as follows:

|

(a)

|

The net deferred

gain (loss) resulting from investments, other

experience and changes in assumptions.

|

|

(b)

|

The prior service

effect of plan amendments deferred for recognition

over remaining service.

|

|

(c)

|

The balance of the

initial difference between assets and obligations

deferred for recognition over a 15-year

period.

|

Top

of page

Note 11. Common

Stock: The Company

increased its quarterly common stock dividend from 25 cents

per share to 27.5 cents, effective with the dividend payment

in June 1997.

In 1998, the Company

repurchased 0.4 million shares on the open market at an

aggregate purchase price of $14 million. In 1997, the

Company repurchased 1.3 million shares from Ford Motor

Company and another 0.2 million shares on the open market at

an aggregate purchase price of $75 million. The Company

repurchased 0.8 million shares on the open market at an

aggregate purchase price of $34 million in 1996. All of the

acquired shares are held as common stock in

treasury.

In 1997, the Company issued

3.75 million shares of its common stock to an employee

benefits trust to fund obligations of employee benefit and

compensation plans, principally retirement savings plans.

Shares of the stock held by this trust are not used in the

calculation of earnings per share until allocated to a

benefit plan.

Note 12. Shareholders' Rights

Plan: The Company

has a Shareholders' Rights Plan which it first adopted in

1986. The Rights Plan provides that each share of the

Company's common stock has associated with it a stock

purchase right. The Rights Plan becomes operative when a

person or entity acquires 15 percent of the Company's common

stock or commences a tender offer to purchase 20 percent or

more of the Company's common stock without the approval of

the Board of Directors.

Note 13. Employee Stock

Plans: Under the

Company's stock incentive and option plans, officers and

other eligible employees may be awarded stock options, stock

appreciation rights and restricted stock. Under the

provisions of the stock incentive plan, up to one percent of

the Company's outstanding shares of common stock at the end

of the preceding year is available for issuance under the

plan each year. At December 31, 1998, there were no shares

of common stock available for grant and 1,234,875 options

exercisable under the plans.

The Company accounts for

stock options in accordance with APB Opinion No. 25 and

related interpretations. No compensation expense has been

recognized for stock options since the options have exercise

prices equal to the market price of the Company's common

stock at the date of grant.

Options outstanding at

December 31, 1998, have exercise prices between $15.94 and

$79.81 and a weighted-average remaining life of 8 years. The

weighted-average fair value of options granted was $18.61

per share in 1998 and $14.94 per share in 1997. The fair

value of each option was estimated on the date of grant

using a risk-free interest rate of 5.6 percent in 1998 and

6.4 percent in 1997, current annual dividends, expected

lives of 10 years and expected volatility of 34 percent. A

fair-value method of accounting for awards subsequent to

January 1, 1996, would have had no material effect on

results of operations.

Top

of page

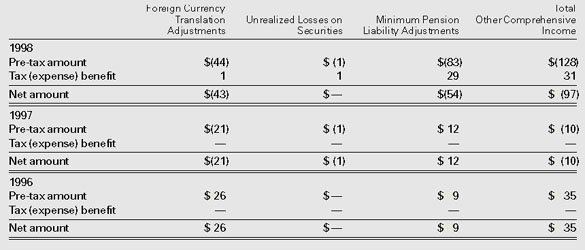

Note 14.

Comprehensive Income: Effective

January 1, 1998, the Company adopted SFAS No. 130, a new

accounting rule which requires companies to report

comprehensive income. Comprehensive income includes net

income and all other nonowner changes in equity during a

period.

The tax

effect on other comprehensive income is as

follows:

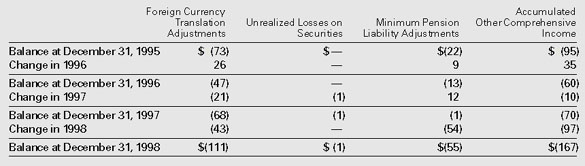

The components of

accumulated other comprehensive income are as

follows:

Top

of page

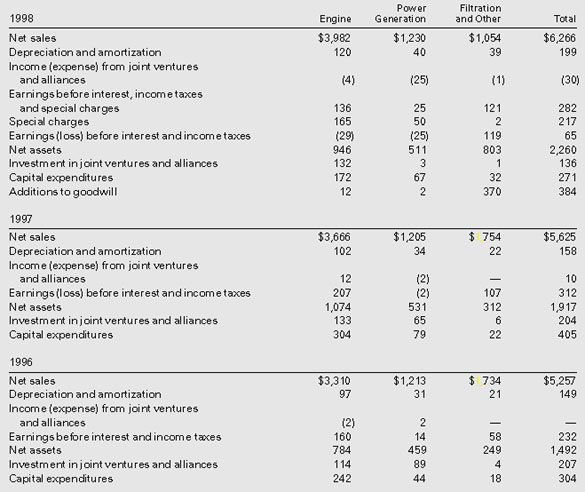

Note 15. Segments of the Business:

Effective for 1998

annual reporting, the Company adopted SFAS No. 131 on

segment reporting. Under the provisions of the new standard,

Cummins has three reportable segments: Engine, Power

Generation, and Filtration and Other. The engine segment

produces engines and parts for sale to customers in

automotive and industrial markets. The engines are used in

trucks of all sizes, buses and recreational vehicles, as

well as various industrial applications including

construction, mining, agriculture, marine, rail and

military. The power generation segment is the Company's

power systems supplier, selling engines, generator sets and

alternators. The filtration and other segment includes sales

of filtration products and exhaust systems, turbochargers

and company-owned distributors.

The Company's reportable

segments are organized according to products and the markets

they each serve. This business structure was designed to

focus efforts on providing enhanced service to a wide range

of customers.

The accounting policies of

the segments are the same as those described in the summary

of significant accounting policies except that the Company

evaluates performance based on earnings before interest and

income taxes and on net assets, and, therefore, no

allocation of debt-related items and income taxes is made to

the individual segments.

Operating segment

information is as follows:

Top

of page

Reconciliation to

Consolidated Financial Statements:

Summary geographic

information is listed below:

(a) Net sales are attributed

to countries based on location of customer.

Revenues from the Company's

largest customer represent approximately $1.1 billion of the

Company's net sales in 1998. These sales are included in the

engine and filtration and other segments.

Top

of page

Note 16. Guarantees, Commitments

and Other Contingencies:

At December 31, 1998, the Company had the following minimum

rental commitments for noncancelable operating leases: $41

million in 1999, $38 million in 2000, $30 million in 2001,

$25 million in 2002, $21 million in 2003 and $46 million

thereafter. Rental expense under these leases approximated

$70 million in 1998, $60 million in 1997 and $55 million in

1996.

Commitments under

outstanding letters of credit, guarantees and contingencies

at December 31, 1998, approximated $195 million.

Cummins and its subsidiaries

are defendants in a number of pending legal actions,

including actions related to use and performance of the

Company's products. The Company carries product liability

insurance covering significant claims for damages involving

personal injury and property damage. In the event the

Company is determined to be liable for damages in connection

with actions and proceedings, the unreserved and uninsured

portion of such liability is not expected to be material.

The Company also has been identified as a potentially

responsible party at several waste disposal sites under US

and related state environmental statutes and regulations.

The Company denies liability with respect to many of these

legal actions and environmental proceedings and vigorously

is defending such actions or proceedings. The Company has

established reserves that it believes are adequate for its

expected future liability in such actions and proceedings

where the nature and extent of such liability can be

estimated reasonably based upon presently available

information.

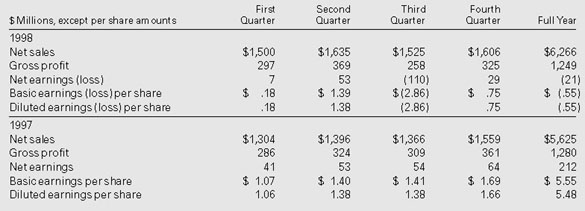

Note 17. Quarterly Financial Data

(unaudited):

Earnings per share for the

first three quarters of 1997 have been restated to reflect

the adoption of SFAS No. 128 as disclosed in Note

1.

Top

of page

Responsibility

for Financial Statements

Management is responsible

for the preparation of the Company's consolidated financial

statements and all related information appearing in this

Report. The statements and notes have been prepared in

conformity with generally accepted accounting principles and

include some amounts which are estimates based upon

currently available information and management's judgment of

current conditions and circumstances. The Company engaged

Arthur Andersen llp, independent public accountants, to

examine the consolidated financial statements. Their report

appears on this page.

To provide reasonable

assurance that assets are safeguarded against loss from

unauthorized use or disposition and that accounting records

are reliable for preparing financial statements, management

maintains a system of accounting and controls, including an

internal audit program. The system of accounting and

controls is improved and modified in response to changes in

business conditions and operations and recommendations made

by the independent public accountants and the internal

auditors.

The Board of Directors has

an Audit Committee whose members are not employees of the

Company. The committee meets periodically with management,

internal auditors and representatives of the Company's

independent public accountants to review the Company's

program of internal controls, audit plans and results, and

the recommendations of the internal and external auditors

and management's responses to those

recommendations.

Top

of page

Report

of Independent Public Accountants

To the Shareholders and

Board of Directors of Cummins Engine Company,

Inc.:

We have audited the

accompanying consolidated statement of financial position of

Cummins Engine Company, Inc., (an Indiana corporation) and

subsidiaries as of December 31, 1998 and 1997, and the

related consolidated statements of earnings, cash flows and

shareholders' investment for each of the three years in the

period ended December 31, 1998. These financial statements

are the responsibility of the Company's management. Our

responsibility is to express an opinion on these financial

statements based on our audits.

We conducted our audits in

accordance with generally accepted auditing standards. Those

standards require that we plan and perform the audit to

obtain reasonable assurance about whether the financial

statements are free of material misstatement. An audit

includes examining, on a test basis, evidence supporting the

amounts and disclosures in the financial statements. An

audit also includes assessing the accounting principles used

and significant estimates made by management, as well as

evaluating the overall financial statement presentation. We

believe that our audits provide a reasonable basis for our

opinion.

In our opinion, the

financial statements referred to above present fairly, in

all material respects, the financial position of Cummins

Engine Company, Inc., and subsidiaries as of December 31,

1998 and 1997, and the results of their operations and their

cash flows for each of the three years in the period ended

December 31, 1998, in conformity with generally accepted

accounting principles.

Chicago, Illinois

January 26, 1999

Top

of page

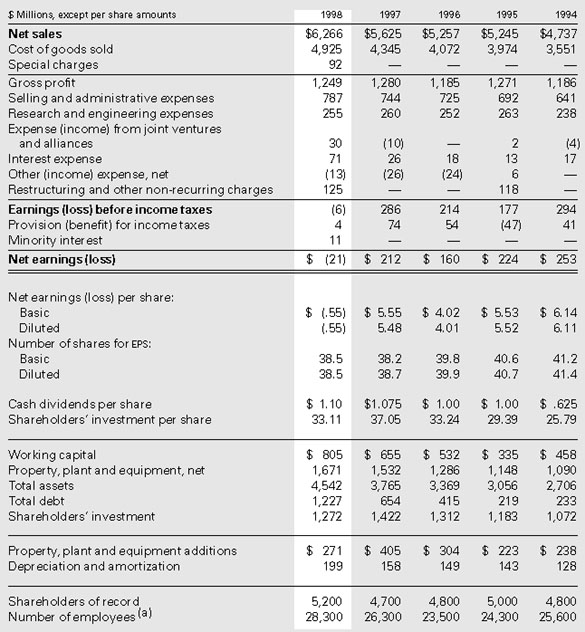

Cummins

Engine Company, Inc.

Five-Year Supplemental Data

(a) Represents the number of

employees at year-end. At December 31, 1998, number of

employees included 2,600 employees of Nelson Industries,

Inc., which was acquired in January 1998. At December 31,

1997, number of employees included 2,800 employees of

Cummins India Limited, which was consolidated in the fourth

quarter of 1997.

Earnings per share for 1994

through 1996 have been restated to reflect the adoption of

SFAS No. 128 as disclosed in Note 1 to the Consolidated

Financial Statements.

Top

of page

|