|

In the United States, our foremost challenge

was to improve new sales growth through

better execution on the distribution side of

our business model. We remain convinced

there are tremendous opportunities for our

business in both markets. Last year, I said

that I believed we could do better. And in

2005, we did. Both Aflac Japan and Aflac

U.S. achieved their sales and financial targets.

In the process, Aflac Incorporated had

another record year.

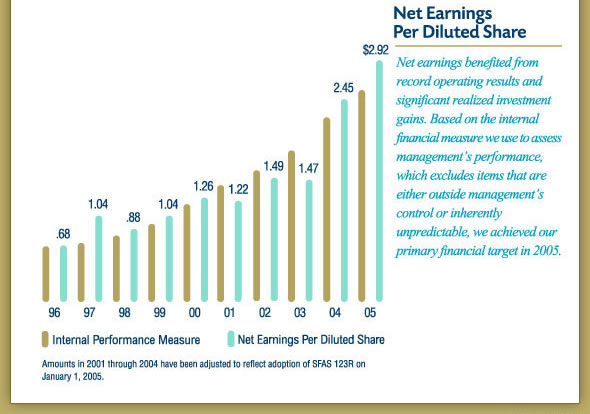

Total revenues surpassed the $14 billion

mark, and net earnings were a record $1.5

billion, or $2.92 per diluted share, in 2005.

Net earnings for the year benefited from the

strong underlying growth of our operations

and an unusually high level of realized

investment gains, compared with 2004.

Most importantly, we again met the primary

financial objective we use internally to assess

the growth of our business. We have

consistently defined that objective as the

growth of net earnings per diluted share,

excluding items that are inherently

unpredictable. We feel this objective is a

valuable measure for judging the

effectiveness of management. And we

believe achieving our objective is the

primary driver of shareholder value.

Consistently repurchasing our shares and

increasing cash dividends are also

components of improving value for our

shareholders. Using excess capital to buy our

shares has been a good investment that has

enhanced our per-share results. Since

initiating our share repurchase program in

1994, we have bought shares every quarter.

In 2005 we purchased 10 million shares,

bringing the total number of shares we have

acquired to more than 187 million since the

program's inception. We also increased the

cash dividend in 2005, marking the 23rd

consecutive year of cash dividend increases.

Cash dividends paid per share in 2005 were

15.8% higher than in 2004.

Aflac Japan was an important contributor to

our record year. We achieved our sales

target, and the persistency of our business

was even better than in 2004. Premium

income, net investment income and

therefore, revenues, surpassed our

expectations. In addition, Aflac Japan's

benefit ratio continued to improve as we

expected, producing higher margins and

solid earnings growth in 2005.

Japan's insurance market has continually

evolved since we entered the country in

1974. Once a market geared to traditional

life insurance coverage, several factors have

caused the demand for our type of products

to emerge as the fastest growing category in

the insurance industry. As a result, more

companies have recognized the

opportunities we have seen for decades,

particularly in the medical insurance area.

Although the market has become more

crowded with supplemental insurance

products, we believe our products represent

a great value to consumers.

To stand out even more in Japan's

competitive market, we introduced two new

medical products as well as a new cancer

product in 2005. These new products

energized our sales force, engaged more

consumers, and helped us reach our sales

target by offering new benefits to the

market. Our sales efforts in Japan also

benefited from aggressive television

advertising. Our advertising continued to

feature the Aflac Duck and focus on our

position as the number one seller of medical

insurance. We believe that consumers prefer

to purchase products from a company that is

the leader in its market. That number one

status, combined with new products and our

reputation for innovation and affordability,

led to a 27.1% increase in medical sales for

the year.

|